As of February 2, 2026, the artificial intelligence industry has officially reached its thermal breaking point. What was once a niche engineering challenge—cooling the massive compute clusters that power large language models—has become the primary bottleneck for the global expansion of AI. The transition from traditional air cooling to mainstream liquid cooling is no longer a strategic choice for data center operators; it is a physical necessity. With the recent debut of NVIDIA (NASDAQ: NVDA) Blackwell and the upcoming deployment of the Rubin architecture, the sheer density of heat generated by these silicon behemoths has rendered the fans and air-conditioning units of the past decade obsolete.

This shift marks a fundamental transformation in the anatomy of the data center. For thirty years, the industry relied on "cold aisles" and high-powered fans to whisk away heat. However, as AI chips breach the 1,000-watt barrier per component, the physics of air—a notoriously poor conductor of heat—have failed. Today, the world’s largest cloud providers, including Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN), and Alphabet (NASDAQ: GOOGL), are racing to retrofit existing facilities and construct massive "AI Superfactories" built entirely around liquid loops, signaling the most significant infrastructure overhaul in the history of modern computing.

The Physics of Rubin: Why Air Finally Failed

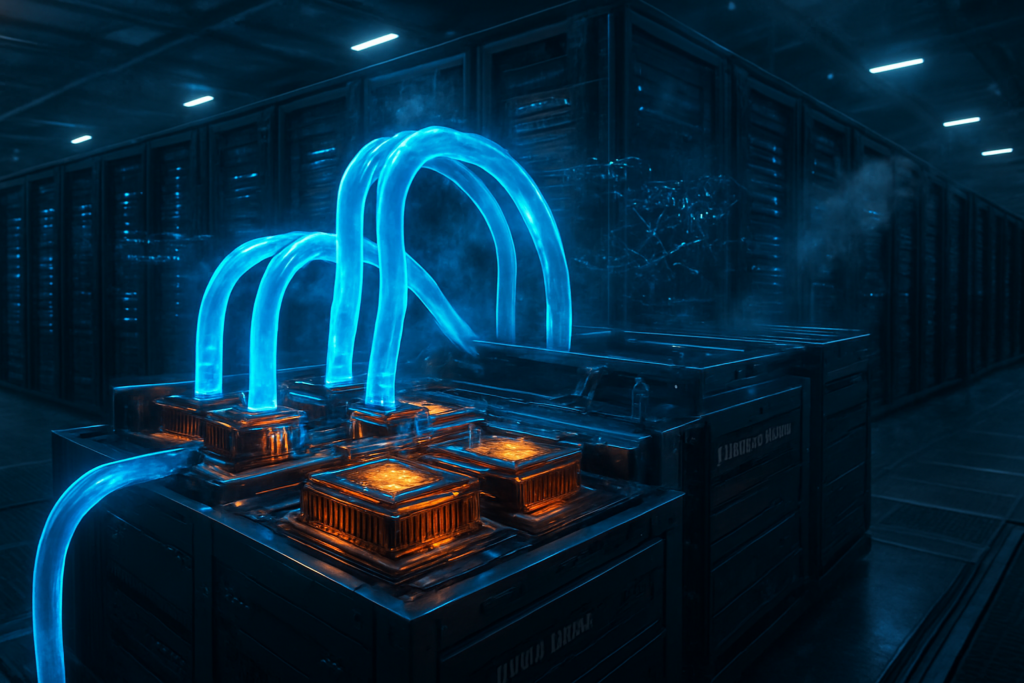

The technical requirements for the latest generation of AI hardware have shattered previous industry standards. While the NVIDIA Blackwell B200 GPUs, which dominated throughout 2025, pushed Thermal Design Power (TDP) to a staggering 1,200 watts per chip, the recently unveiled Rubin R100 platform has moved the goalposts even further. Early production units of the Rubin architecture, slated for volume shipment in the second half of 2026, are pushing individual GPU TDPs toward 2,000 watts. When these chips are clustered into the Vera Rubin NVL72 rack configuration, the power density reaches an eye-watering 140kW to 200kW per rack. To put this in perspective, a standard enterprise server rack just five years ago typically consumed between 5kW and 10kW.

To manage this heat, the industry has standardized on Direct-to-Chip (DTC) cooling and, increasingly, immersion cooling. DTC technology uses "cold plates"—high-conductivity copper blocks—that sit directly atop the GPU and memory stacks. A dielectric or treated water-based fluid circulates through these plates, absorbing heat far more efficiently than air. The technical leap with the Rubin platform is its mandate for "warm water cooling." By utilizing liquid at 45°C (113°F), data centers can eliminate energy-intensive mechanical chillers, instead using simple dry coolers to dissipate heat into the ambient air. This breakthrough has allowed leading server manufacturers like Super Micro Computer (NASDAQ: SMCI) and Dell Technologies (NYSE: DELL) to design systems that are not only more powerful but significantly more energy-efficient, with some facilities reporting Power Usage Effectiveness (PUE) ratings as low as 1.05.

The Infrastructure Gold Rush: Beneficiaries of the Liquid Shift

The forced migration to liquid cooling has created a new class of high-growth infrastructure giants. Vertiv (NYSE: VRT) and Schneider Electric (OTCPK: SBGSY) have emerged as the primary "arms dealers" in this transition. Vertiv, in particular, has seen its market position solidify through its modular liquid-cooling units that can be rapidly deployed in existing data centers. Schneider Electric’s 2025 acquisition of Motivair has allowed it to offer end-to-end "liquid-ready" architectures, from the Cooling Distribution Units (CDUs) to the manifold systems that snake through the server racks.

This transition has also created a competitive divide among colocation providers. Companies like Equinix (NASDAQ: EQIX) and Digital Realty (NYSE: DLR) that moved early to install heavy-duty piping and liquid-loop infrastructure are now the only facilities capable of hosting the next generation of AI training clusters. Smaller data center operators that failed to invest in liquid-ready footprints are finding themselves locked out of the lucrative AI market, as their facilities simply cannot provide the power density or cooling required for Blackwell or Rubin hardware. This infrastructure "moat" is reshaping the real estate dynamics of the tech industry, favoring those with the capital and engineering foresight to embrace a "wet" data center environment.

Sustainability and the Global Power Paradigm

Beyond the immediate technical hurdles, the adoption of liquid cooling is a double-edged sword for the environment. On one hand, liquid cooling is vastly more efficient than air cooling, potentially reducing a data center’s cooling-related energy consumption by up to 90%. This efficiency is critical as the total power demand of the AI sector is projected to rival that of small nations by the end of the decade. By moving to warm water cooling, operators can significantly lower their carbon footprint and water consumption, as traditional evaporative cooling towers are no longer strictly necessary.

However, the sheer scale of the new AI Superfactories presents a daunting challenge. The move to liquid cooling allows for much higher density, which in turn encourages the construction of even larger facilities. We are now seeing the rise of "gigawatt-scale" data center campuses. Concerns are mounting among local governments and environmental groups regarding the massive localized power draw and the potential for "thermal pollution"—the release of massive amounts of waste heat into the environment. While the technology is more efficient per unit of compute, the total volume of compute is growing so rapidly that it may offset these gains, keeping the industry in a perpetual race against its own energy demands.

The Road to 600kW: What Comes After Rubin?

As we look toward 2027 and 2028, the trajectory of AI hardware suggests that even current liquid cooling methods may eventually reach their limits. Experts predict that the successor to Rubin, already whispered about in R&D circles, will likely push rack densities toward 600kW. At these levels, "phase-change" cooling—where the liquid refrigerant actually boils and turns to gas as it absorbs heat—is expected to become the new frontier. This technology, currently in testing by specialized firms like nVent (NYSE: NVT), promises an even greater step-change in thermal management.

Furthermore, we are beginning to see the first practical applications of "district heating" from AI data centers. In northern Europe and parts of North America, the high-grade waste heat (reaching 60°C or more) from liquid-cooled AI clusters is being piped into local municipal heating systems to warm homes and businesses. This "circular heat" economy could transform data centers from energy sinks into valuable public utilities, providing a social and economic justification for their immense power consumption. The challenge will remain in the global supply chain, as the demand for specialized components like quick-disconnect manifolds and high-pressure pumps currently exceeds manufacturing capacity by nearly 40%.

A Liquid Future for the Intelligence Age

The mainstreaming of liquid cooling in early 2026 represents a pivotal moment in the history of computing. It is the point where the digital and the physical have collided most violently, forcing a total redesign of how we build the brains of the AI era. The transition driven by NVIDIA’s relentless release cycle—from Hopper to Blackwell and now to Rubin—has permanently altered the data center landscape. Air cooling, once the bedrock of the industry, is now a relic of a lower-density past, reserved for legacy workloads and basic enterprise tasks.

As we move forward, the success of AI companies will be measured not just by their algorithms or their data, but by their thermal engineering. In the coming months, watch for the first full-scale deployments of "Vera Rubin" clusters and the quarterly earnings of infrastructure providers like Vertiv and Schneider Electric, which have become the barometers for AI’s physical growth. The era of the "cool and quiet" data center is over; the era of the high-density, liquid-powered AI factory has arrived.

This content is intended for informational purposes only and represents analysis of current AI developments.

TokenRing AI delivers enterprise-grade solutions for multi-agent AI workflow orchestration, AI-powered development tools, and seamless remote collaboration platforms.

For more information, visit https://www.tokenring.ai/.