Over the past six months, Live Nation’s shares (currently trading at $164.50) have posted a disappointing 5.3% loss, well below the S&P 500’s 3% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Live Nation, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Live Nation Not Exciting?

Despite the more favorable entry price, we don't have much confidence in Live Nation. Here are three reasons there are better opportunities than LYV and a stock we'd rather own.

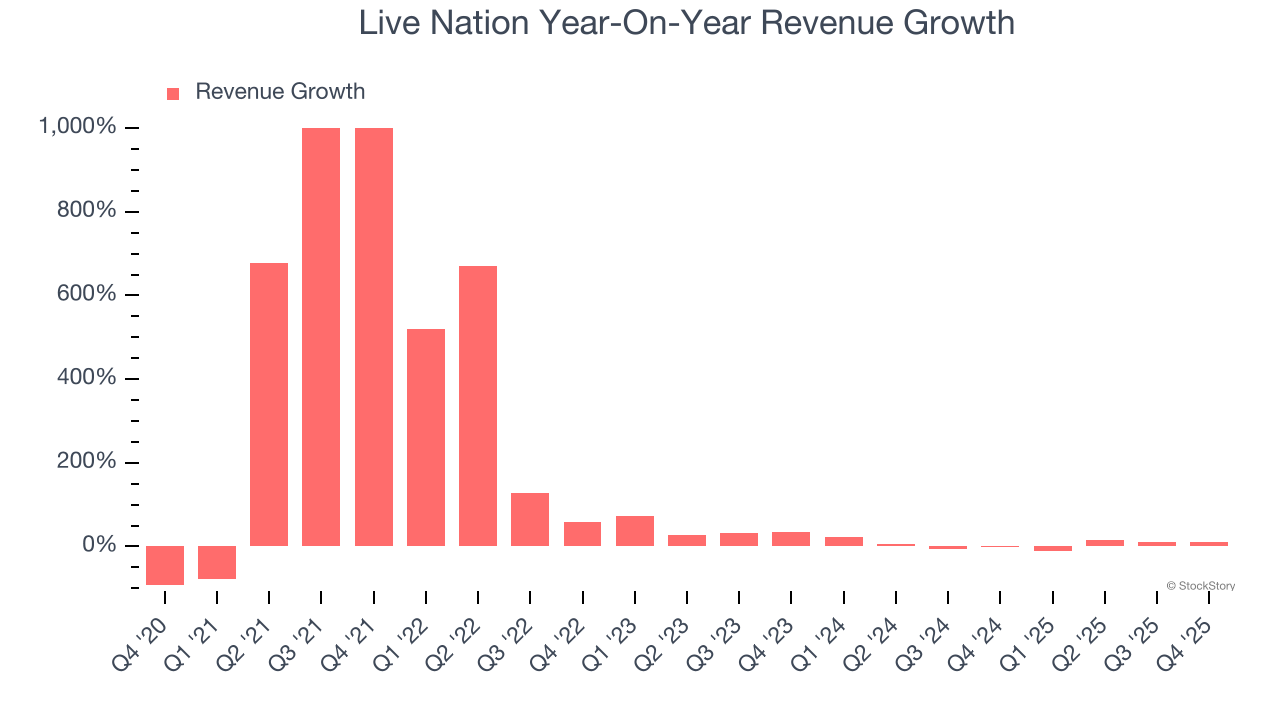

1. Lackluster Revenue Growth

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Live Nation’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 5.3% over the last two years was well below its five-year trend. Note that COVID hurt Live Nation’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

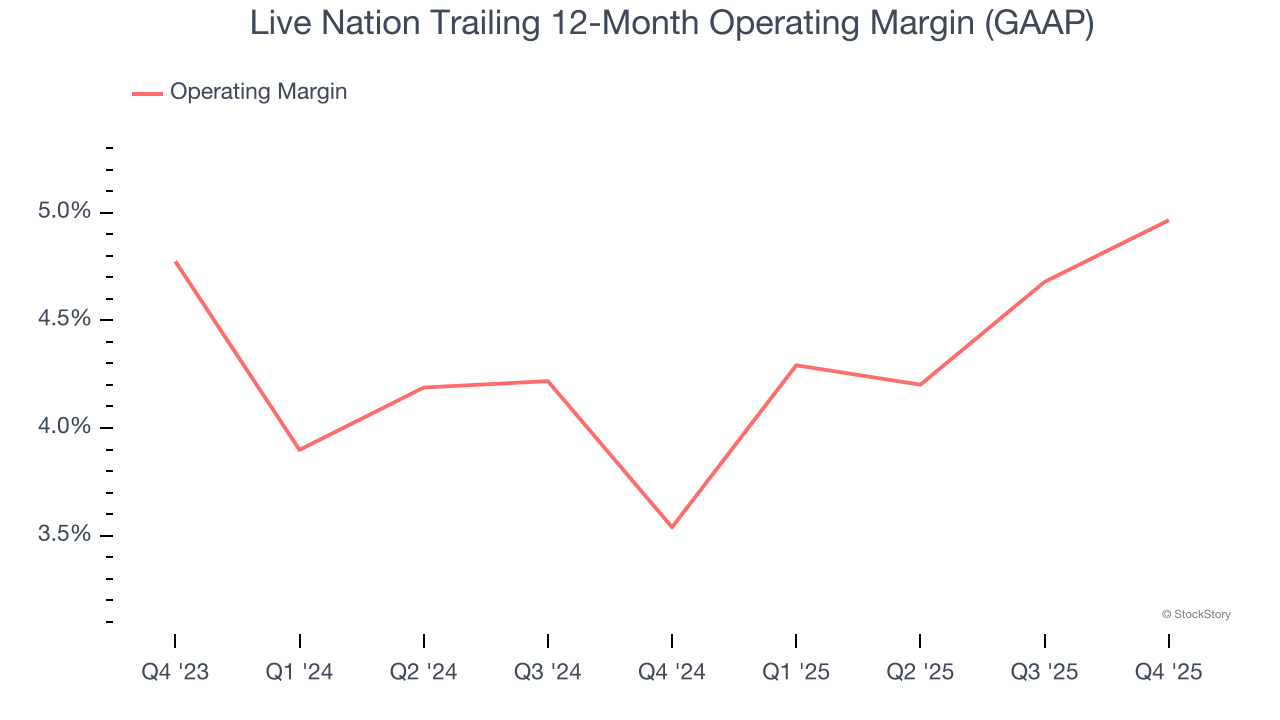

2. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Live Nation’s operating margin has risen over the last 12 months and averaged 4.3% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

3. Cash Flow Margin Set to Decline

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts predict Live Nation’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 6.6% for the last 12 months will decrease to 5.3%.

Final Judgment

Live Nation isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 121.4× forward P/E (or $164.50 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d recommend looking at the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Live Nation

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.