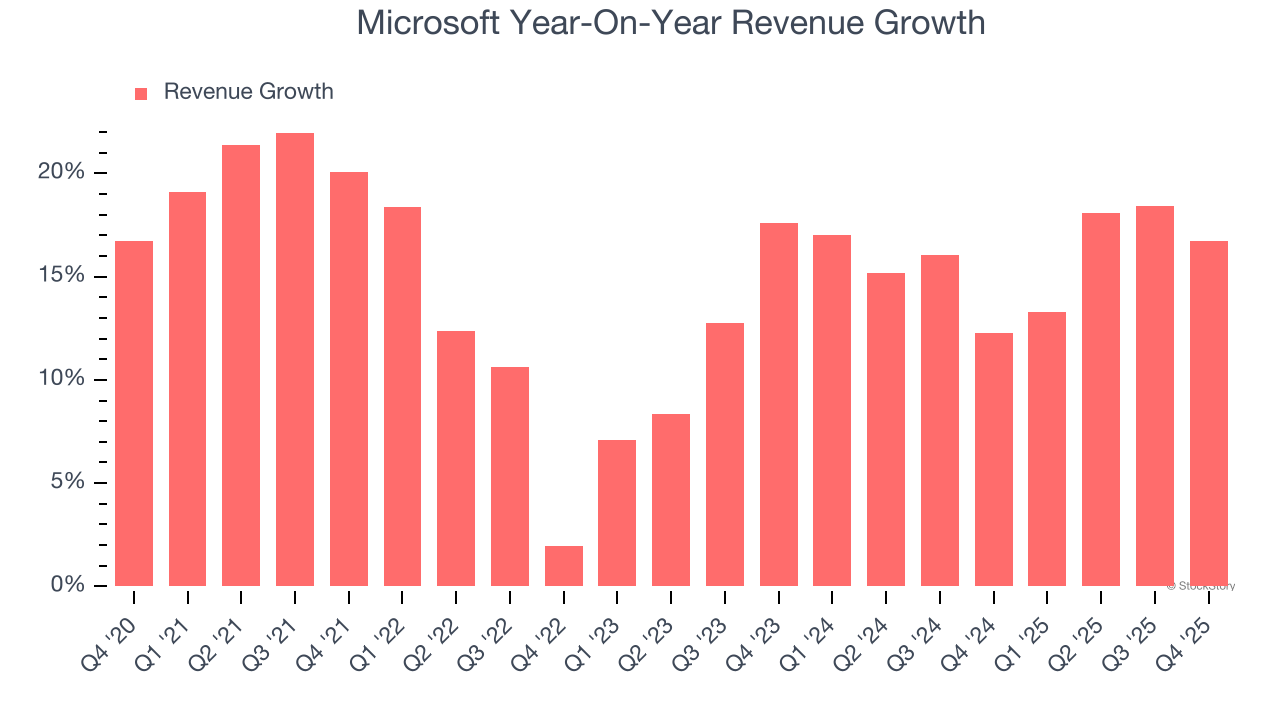

Technology giant Microsoft (NASDAQ: MSFT) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 16.7% year on year to $81.27 billion. Its GAAP profit of $5.16 per share was 34.1% above analysts’ consensus estimates.

Is now the time to buy Microsoft? Find out by accessing our full research report, it’s free.

Microsoft (MSFT) Q4 CY2025 Highlights:

- Revenue: $81.27 billion vs analyst estimates of $80.32 billion (1.2% beat)

- Operating Profit (GAAP): $38.28 billion vs analyst estimates of $36.62 billion (4.5% beat)

- EPS (GAAP): $5.16 vs analyst estimates of $3.85 (34.1% beat, non-GAAP EPS was $4.14 excluding OpenAI impacts)

- Intelligent Cloud Revenue: $0.02 vs analyst estimates of $32.34 billion (1.8% beat, Azure constant-current growth of 38% year-on-year)

- Business Software Revenue: $34.12 billion vs analyst estimates of $33.46 billion (2% beat)

- Personal Computing Revenue: $14.25 billion vs analyst estimates of $15.77 billion (9.7% miss)

- Gross Margin: 68%, in line with the same quarter last year

- Operating Margin: 47.1%, up from 45.5% in the same quarter last year

- Free Cash Flow Margin: 7.2%, down from 9.3% in the same quarter last year

- Market Capitalization: $3.57 trillion

Revenue Growth

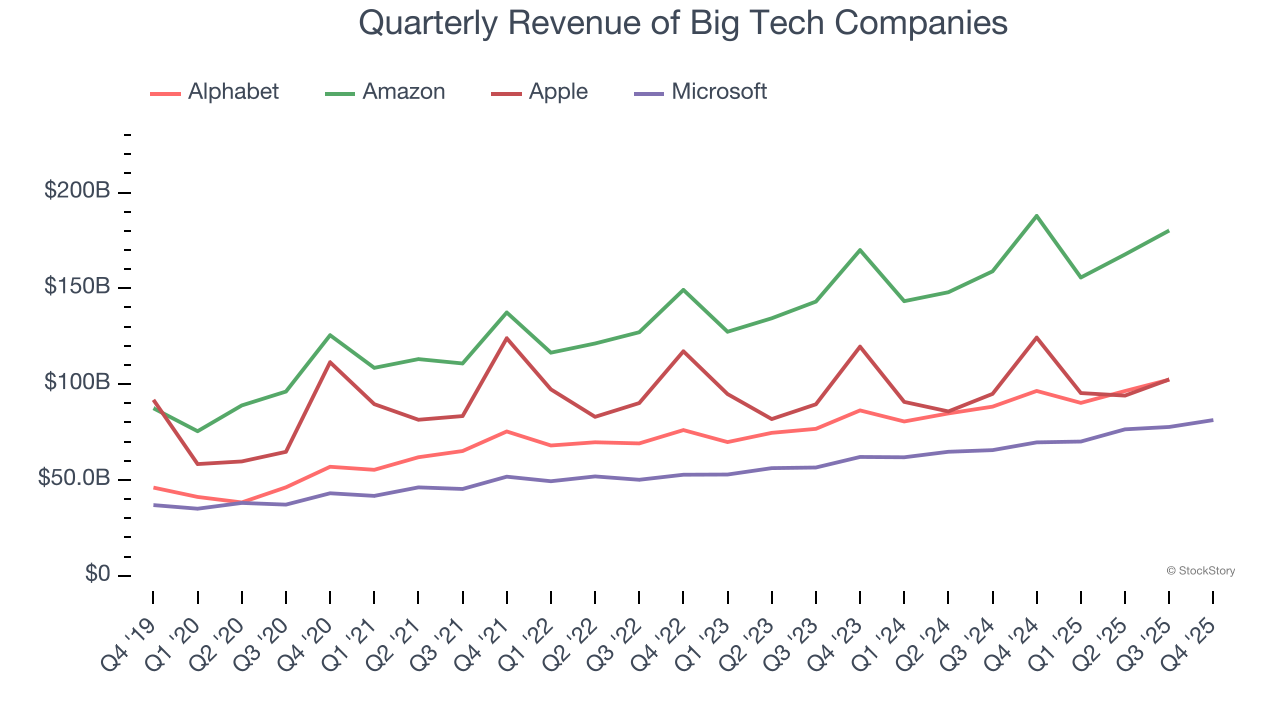

Microsoft proves that huge, scaled companies can still grow quickly. The company’s revenue base of $153.3 billion five years ago has nearly doubled to $305.5 billion in the last year, translating into an exceptional 14.8% annualized growth rate.

Over the same period, Microsoft’s big tech peers Amazon, Alphabet, and Apple put up annualized growth rates of 14.1%, 18.1%, and 9.8%, respectively. Comparing the four is relevant because investors often pit them against each other to derive their valuations. With these benchmarks in mind, we think Microsoft’s price is attractive.

Long-term growth reigns supreme in fundamentals, but for big tech companies, a half-decade historical view may miss emerging trends in AI. Microsoft’s annualized revenue growth of 15.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Microsoft reported year-on-year revenue growth of 16.7%, and its $81.27 billion of revenue exceeded Wall Street’s estimates by 1.2%. Looking ahead, sell-side This projection is admirable for a company of its scale and illustrates the market sees some success for its newer AI-enabling products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

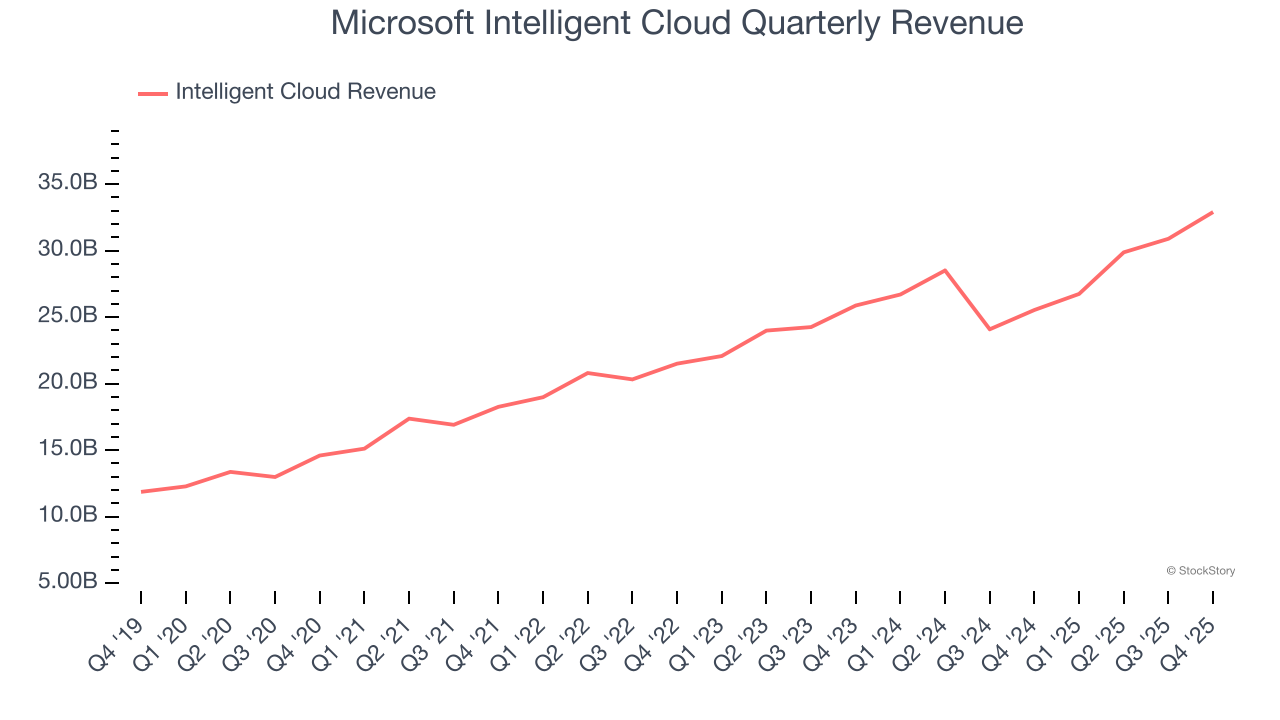

Intelligent Cloud: Azure & Cloud Computing

The most pressing question about Microsoft’s business is how much AI can boost its revenues. The company's cloud computing division, Intelligent Cloud, is one we watch carefully because its Azure platform and server/database offerings could be the biggest beneficiaries of the AI megatrend.

Intelligent Cloud is 39.4% of Microsoft’s total sales and grew at a 17.7% annualized rate over the last five years, faster than its consolidated revenues. The previous two years saw deceleration as it grew by 11.9% annually.

Intelligent Cloud’s 28.8% year-on-year revenue growth exceeded expectations in Q4, beating Wall Street’s estimates by 1.8%.

In terms of market share, Azure is a close second as its run-rate revenue (current quarter’s sales times four) is around $150 billion versus roughly $150 billion and $60 billion for AWS and Google Cloud. If Azure wants to catch up to AWS in the coming years, growth will have to accelerate beyond its current levels.

Key Takeaways from Microsoft’s Q4 Results

Business Services and Intelligent Cloud revenue beat, but Personal Computing missed. EPS, even after removing the impacts of OpenAI, also beat expectations. However, the magnitude of the beat in Intelligent Cloud and Azure's growth rate could be called into question by some investors hoping for stronger results, aided by AI products and services. Zooming out, we think this was still a good print with some key areas of upside. The stock remained flat at $460.92 immediately after reporting.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).