E.W. Scripps has been treading water for the past six months, recording a small loss of 2.7% while holding steady at $2.20.

Is there a buying opportunity in E.W. Scripps, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think E.W. Scripps Will Underperform?

We don't have much confidence in E.W. Scripps. Here are three reasons why we avoid SSP and a stock we'd rather own.

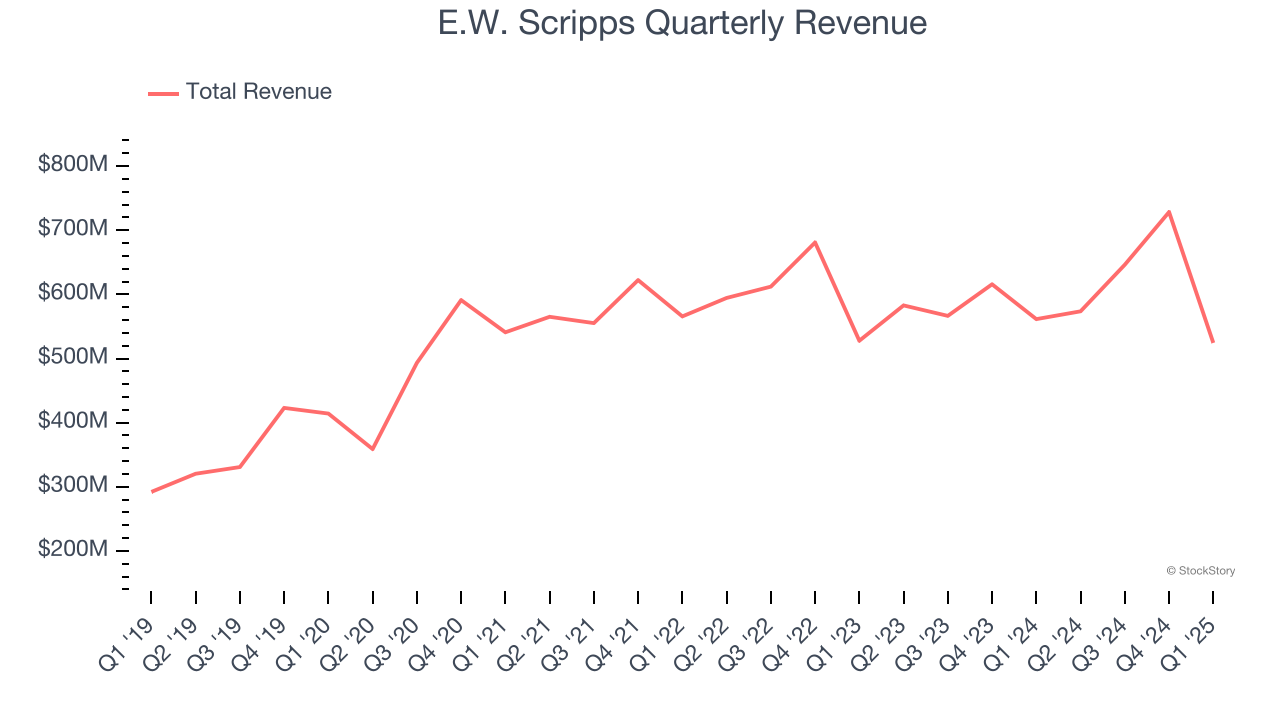

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, E.W. Scripps grew its sales at a 10.7% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

2. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict E.W. Scripps’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 10.9% for the last 12 months will decrease to 3.8%.

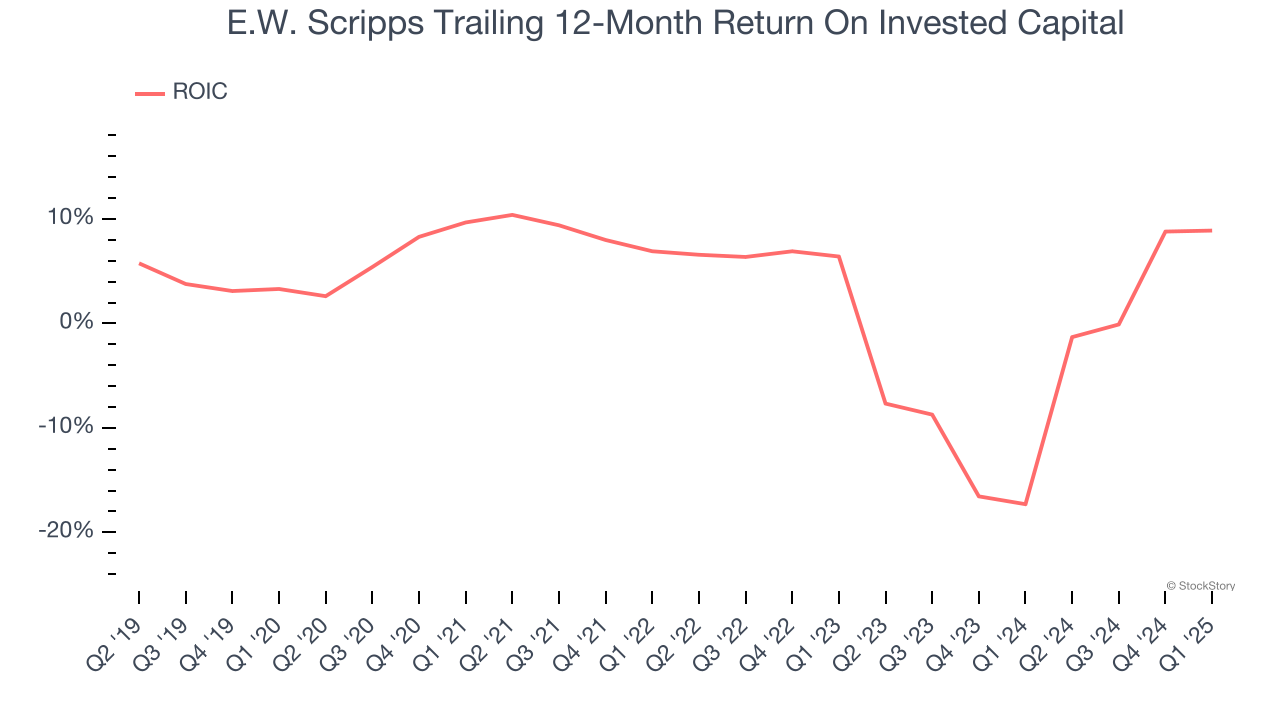

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, E.W. Scripps’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

E.W. Scripps doesn’t pass our quality test. That said, the stock currently trades at 0.7× forward EV-to-EBITDA (or $2.20 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

Stocks We Would Buy Instead of E.W. Scripps

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.