As the Q2 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the beauty and cosmetics retailer industry, including Warby Parker (NYSE: WRBY) and its peers.

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

The 4 beauty and cosmetics retailer stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.2% while next quarter’s revenue guidance was in line.

Luckily, beauty and cosmetics retailer stocks have performed well with share prices up 11.6% on average since the latest earnings results.

Warby Parker (NYSE: WRBY)

Founded in 2010, Warby Parker (NYSE: WRBY) designs, manufactures, and sells eyewear, including prescription glasses, sunglasses, and contact lenses, through its e-commerce platform and physical retail locations.

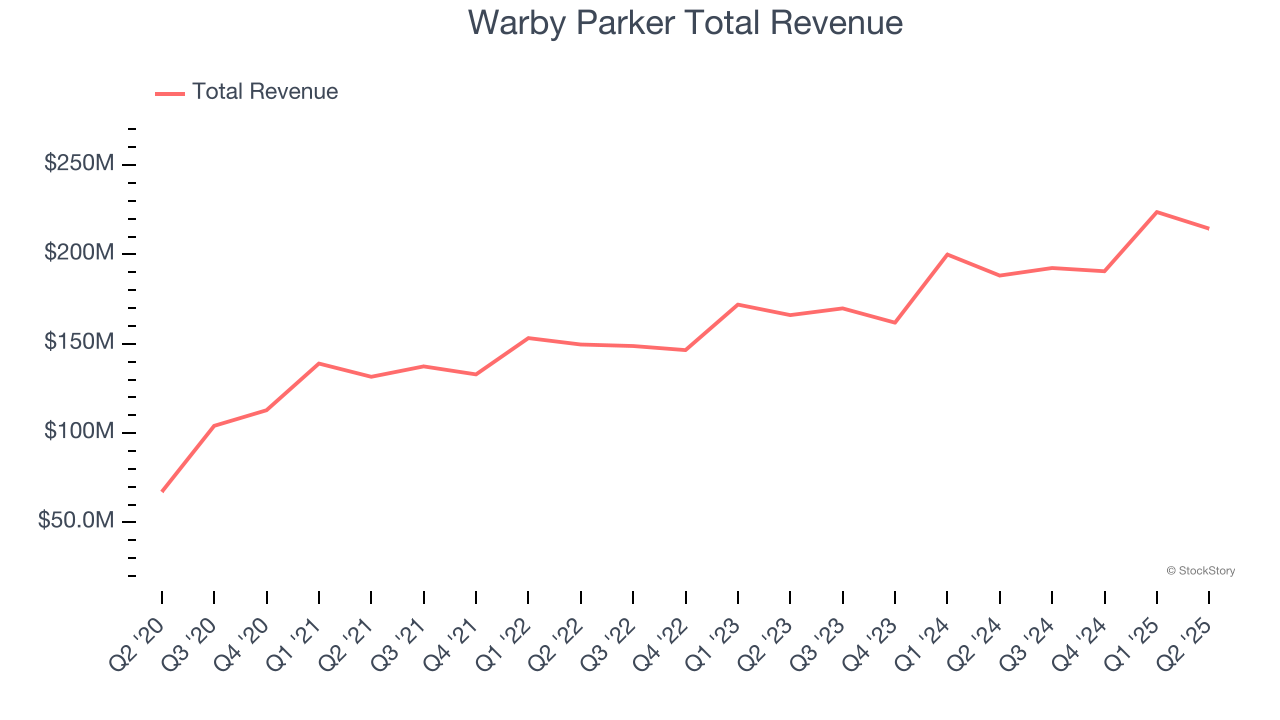

Warby Parker reported revenues of $214.5 million, up 13.9% year on year. This print exceeded analysts’ expectations by 0.7%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

“When Steve joined Warby Parker fourteen years ago as our first CFO, he brought financial rigor, strategic vision, and an unwavering commitment to creating impact both inside and outside of the organization,” says Gilboa.

Warby Parker pulled off the fastest revenue growth but had the weakest full-year guidance update of the whole group. The results were likely priced in, however, and the stock is flat since reporting. It currently trades at $24.50.

Is now the time to buy Warby Parker? Access our full analysis of the earnings results here, it’s free for active Edge members.

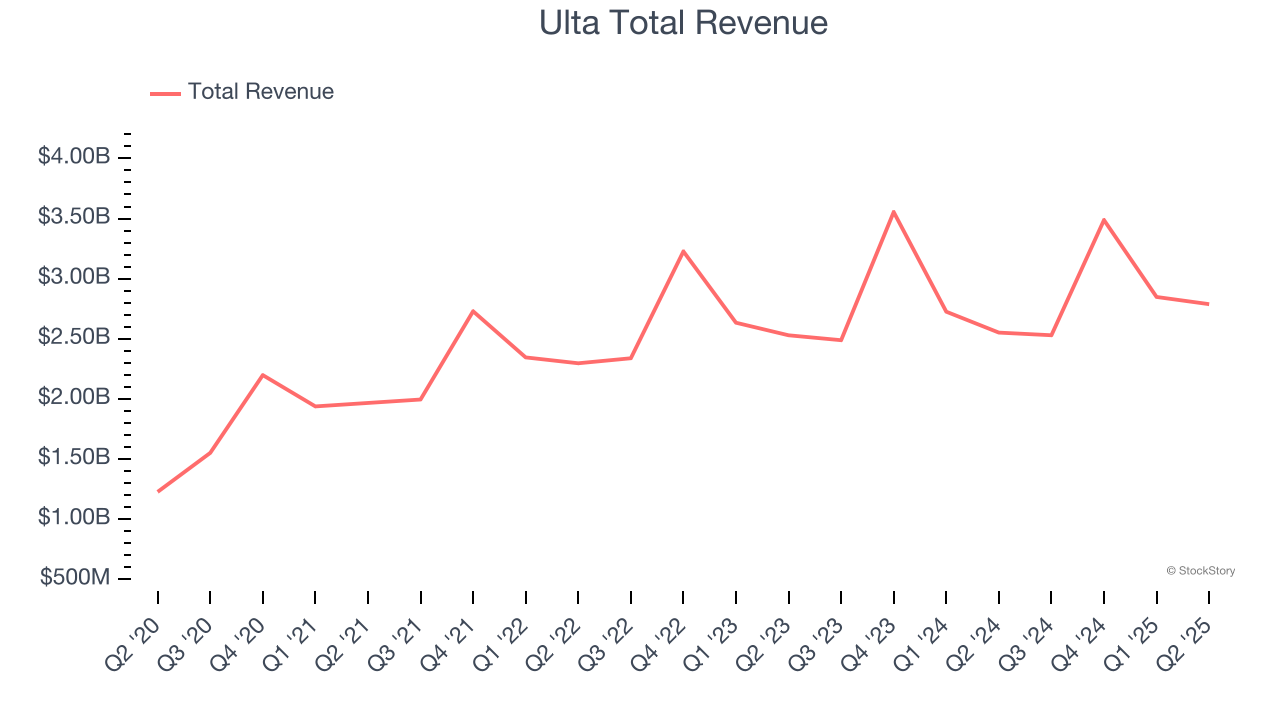

Best Q2: Ulta (NASDAQ: ULTA)

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ: ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Ulta reported revenues of $2.79 billion, up 9.3% year on year, outperforming analysts’ expectations by 4.2%. The business had an exceptional quarter with an impressive beat of analysts’ EBITDA and revenue estimates.

Ulta pulled off the biggest analyst estimates beat and highest full-year guidance raise among its peers. The market seems content with the results as the stock is up 4.9% since reporting. It currently trades at $556.21.

Is now the time to buy Ulta? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: Bath and Body Works (NYSE: BBWI)

Spun off from L Brands in 2020, Bath & Body Works (NYSE: BBWI) is a personal care and home fragrance retailer where consumers can find specialty shower gels, scented candles for the home, and lotions.

Bath and Body Works reported revenues of $1.55 billion, up 1.5% year on year, in line with analysts’ expectations. It was a softer quarter as it posted EPS guidance for next quarter missing analysts’ expectations.

Bath and Body Works delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 18.2% since the results and currently trades at $25.79.

Read our full analysis of Bath and Body Works’s results here.

Sally Beauty (NYSE: SBH)

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE: SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Sally Beauty reported revenues of $933.3 million, flat year on year. This print was in line with analysts’ expectations. Overall, it was a very strong quarter as it also logged a solid beat of analysts’ EBITDA and EPS estimates.

Sally Beauty had the slowest revenue growth among its peers. The stock is up 58.7% since reporting and currently trades at $15.82.

Read our full, actionable report on Sally Beauty here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.