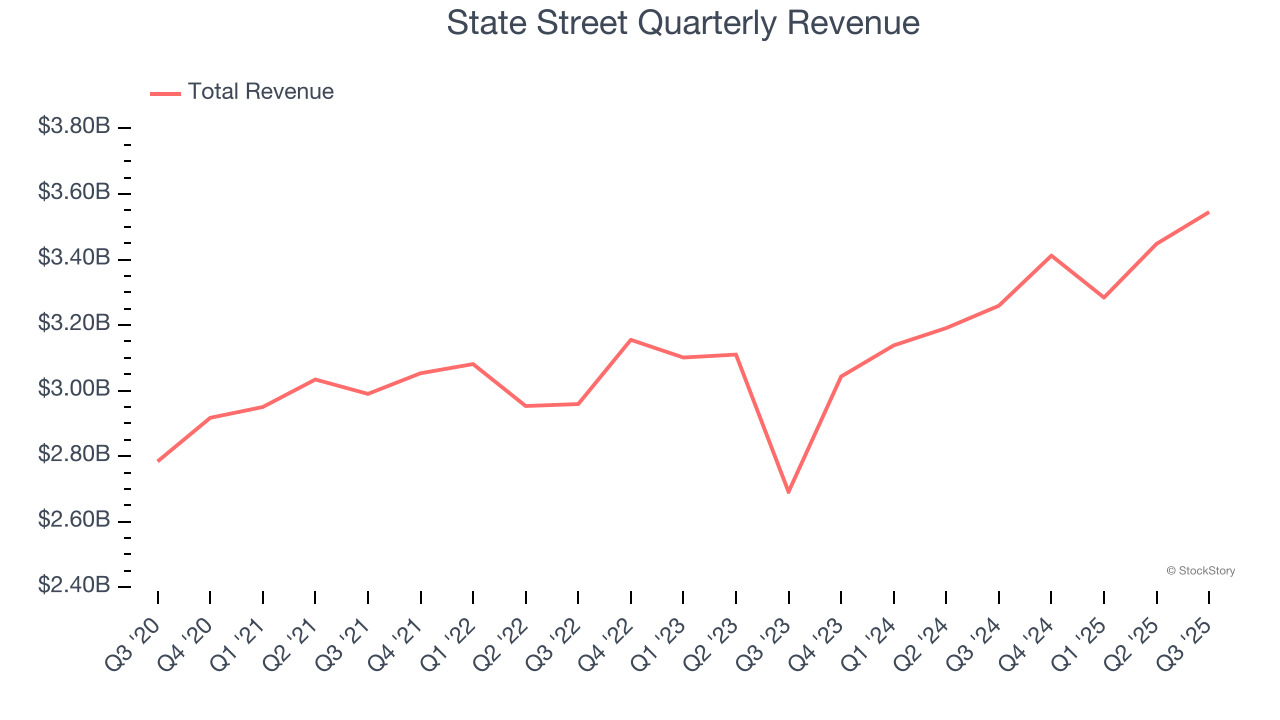

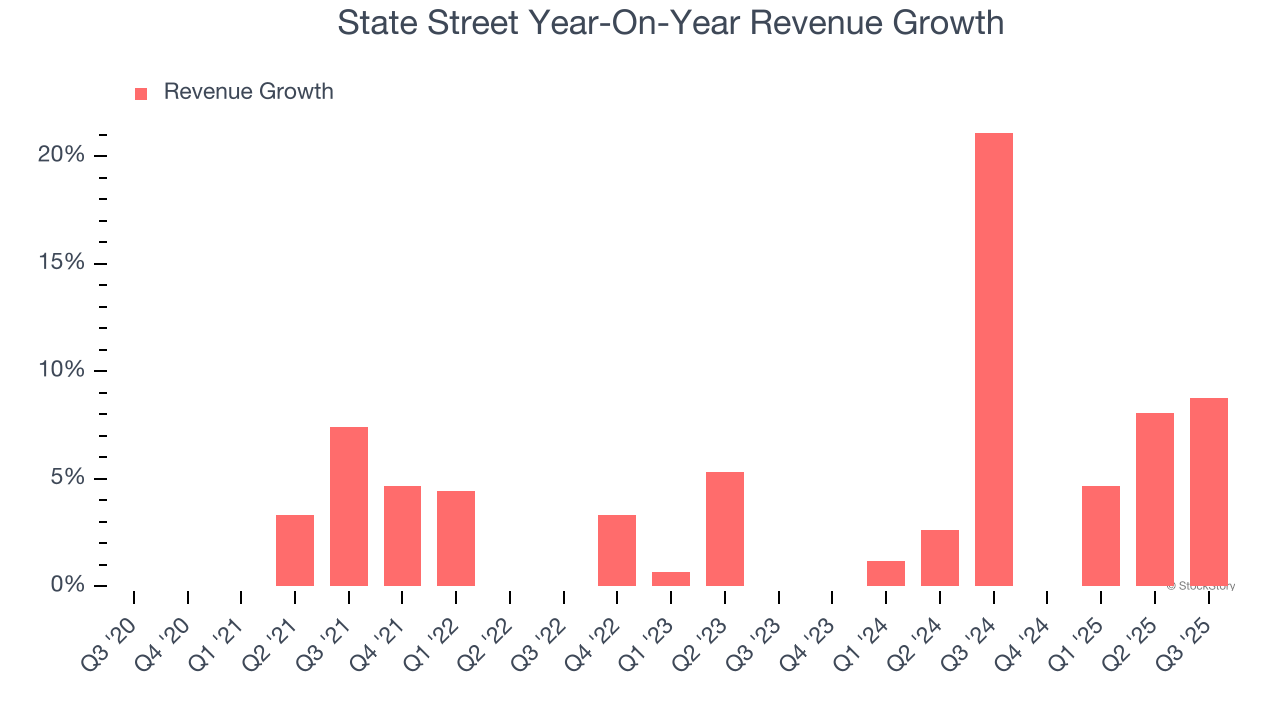

Financial services giant State Street (NYSE: STT) reported revenue ahead of Wall Street’s expectations in Q3 CY2025, with sales up 8.8% year on year to $3.55 billion. Its non-GAAP profit of $2.78 per share was 5% above analysts’ consensus estimates.

Is now the time to buy State Street? Find out by accessing our full research report, it’s free for active Edge members.

State Street (STT) Q3 CY2025 Highlights:

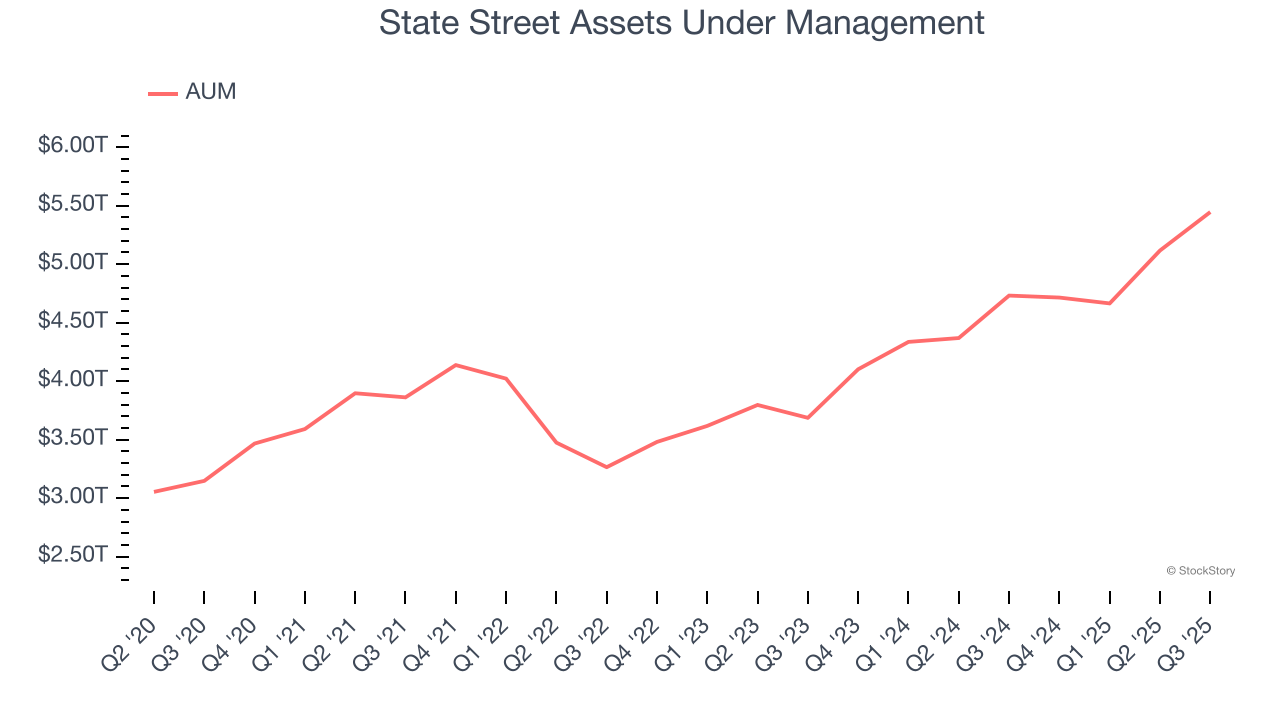

- Assets Under Management: $5.45 trillion vs analyst estimates of $5.17 trillion (15.1% year-on-year growth, 5.4% beat)

- Revenue: $3.55 billion vs analyst estimates of $3.47 billion (8.8% year-on-year growth, 2.3% beat)

- Pre-tax Profit: $1.1 billion (31.1% margin, 19.1% year-on-year growth)

- Adjusted EPS: $2.78 vs analyst estimates of $2.65 (5% beat)

- Market Capitalization: $32.04 billion

Company Overview

Dating back to 1792 when Boston's Long Wharf was the center of global shipping and trade, State Street (NYSE: STT) provides custody, investment management, and other financial services to institutional investors like pension funds, asset managers, and central banks worldwide.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, State Street grew its revenue at a sluggish 3% compounded annual growth rate. This was below our standards and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. State Street’s annualized revenue growth of 6.6% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, State Street reported year-on-year revenue growth of 8.8%, and its $3.55 billion of revenue exceeded Wall Street’s estimates by 2.3%.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Assets Under Management (AUM)

Assets Under Management (AUM) is the cornerstone of a financial firm's investment division, representing all client capital under its stewardship. Management fees on this AUM create reliable, recurring revenue that maintains stability even when investment performance struggles, though prolonged poor returns can eventually affect asset retention and growth.

State Street’s AUM has grown at an annual rate of 7.7% over the last four years, slightly better than the broader financials industry. When analyzing State Street’s AUM over the last two years, we can see that growth accelerated to 16.9% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. Keep in mind that asset growth can be erratic and seasonal, so we don't rely on it too heavily for our business quality analysis.

In Q3, State Street’s AUM was $5.45 trillion, beating analysts’ expectations by 5.4%. This print was 15.1% higher than the same quarter last year.

Key Takeaways from State Street’s Q3 Results

We were impressed by how significantly State Street blew past analysts’ AUM expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 2.7% to $109.92 immediately following the results.

Big picture, is State Street a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.