Howmet currently trades at $114.80 and has been a dream stock for shareholders. It’s returned 268% since December 2019, nearly tripling the S&P 500’s 91.9% gain. The company has also beaten the index over the past six months as its stock price is up 38% thanks to its solid quarterly results.

Is now still a good time to buy HWM? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Are We Positive On HWM?

Inventing the first forged aluminum truck wheel, Howmet (NYSE: HWM) specializes in lightweight metals engineering and manufacturing multi-material components used in vehicles.

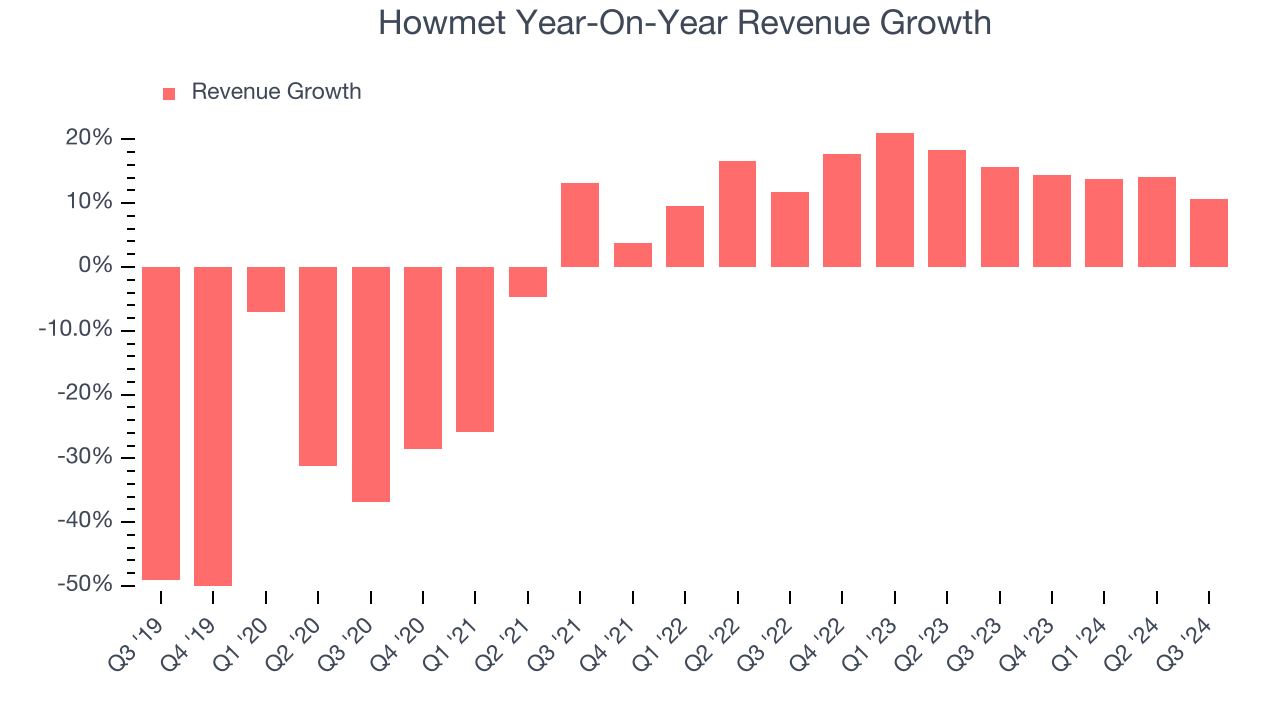

1. Skyrocketing Revenue Shows Strong Momentum

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Howmet’s annualized revenue growth of 15.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

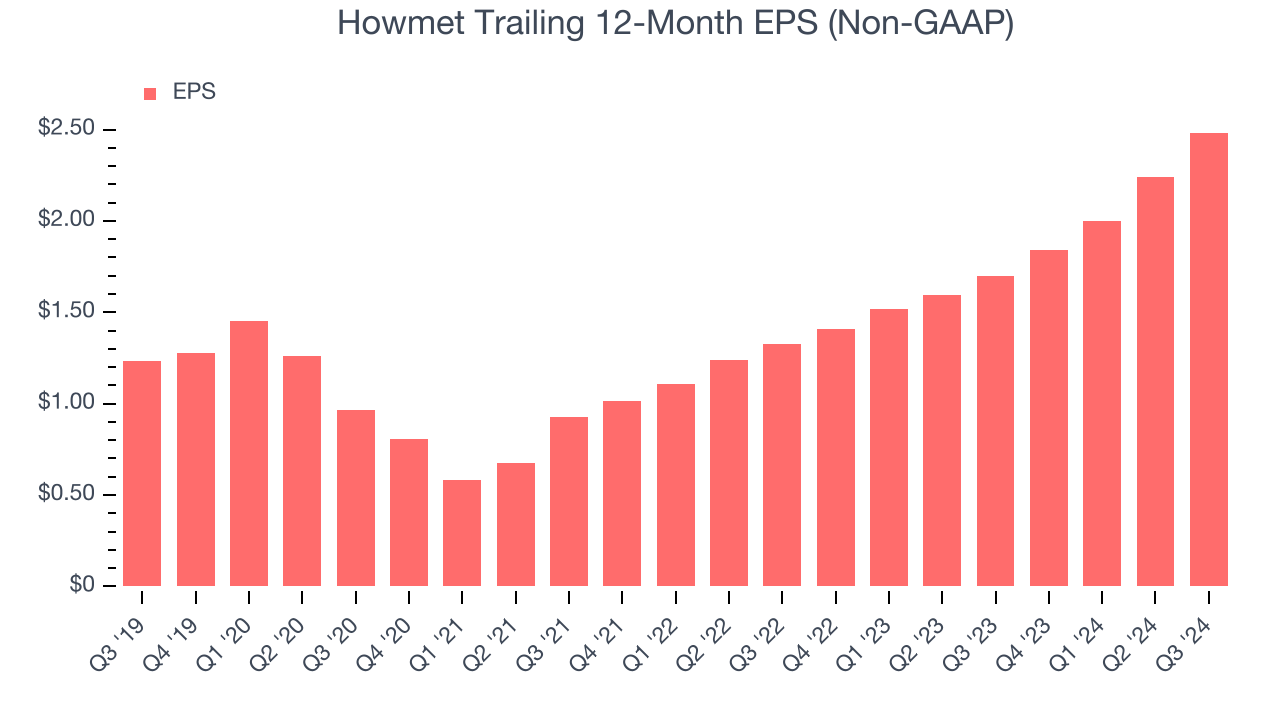

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Howmet’s EPS grew at a spectacular 15.1% compounded annual growth rate over the last five years, higher than its 3.8% annualized revenue declines. This tells us management adapted its cost structure in response to a challenging demand environment.

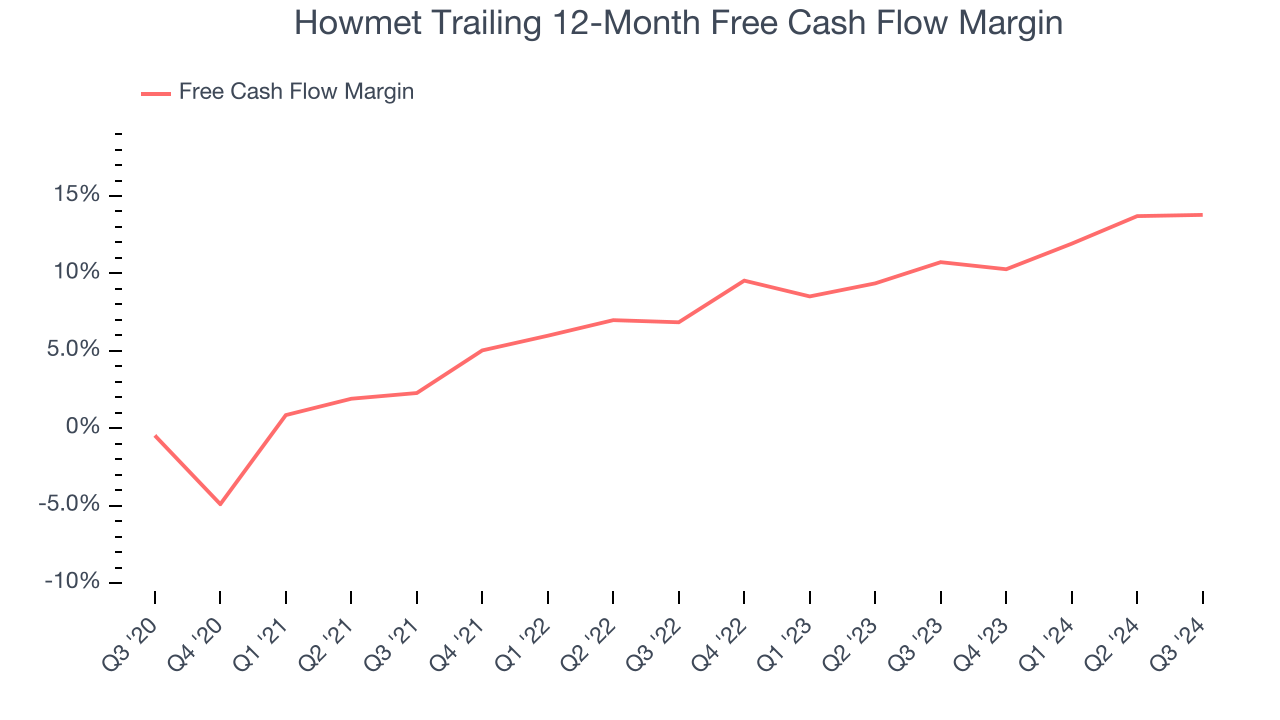

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Howmet’s margin expanded by 14.3 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose by more than its operating profitability. Howmet’s free cash flow margin for the trailing 12 months was 13.8%.

Final Judgment

These are just a few reasons why we think Howmet is a high-quality business, and with its shares outperforming the market lately, the stock trades at 39.3× forward price-to-earnings (or $114.80 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Howmet

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.