CarMax’s 23.1% return over the past six months has outpaced the S&P 500 by 9.7%, and its stock price has climbed to $85.09 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy CarMax, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.Despite the momentum, we don't have much confidence in CarMax. Here are three reasons why KMX doesn't excite us and one stock we'd rather own today.

Why Do We Think CarMax Will Underperform?

Known for its transparent, customer-centric approach and wide selection of vehicles, Carmax (NYSE: KMX) is the largest automotive retailer in the United States.

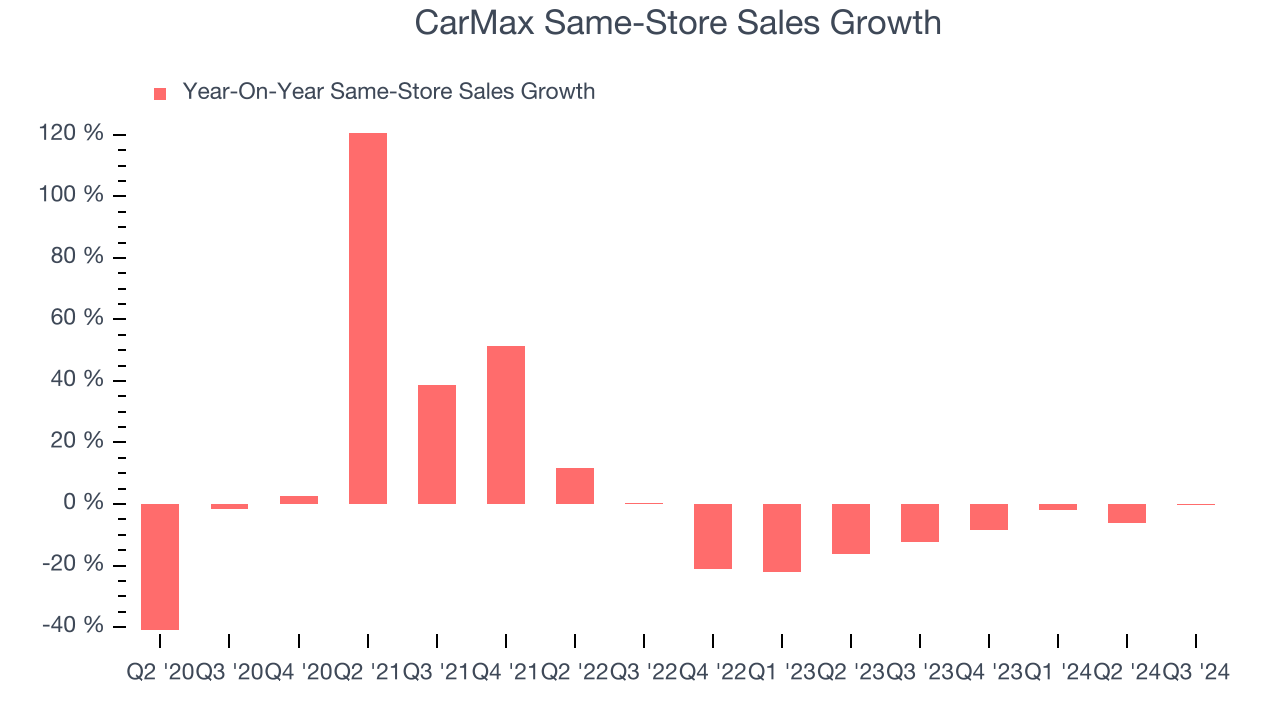

1. Declining Same-Store Sales Indicate Demand Is Evaporating

Same-store sales growth shows the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

CarMax’s demand has been shrinking over the last two years as its same-store sales have averaged 11% annual declines.

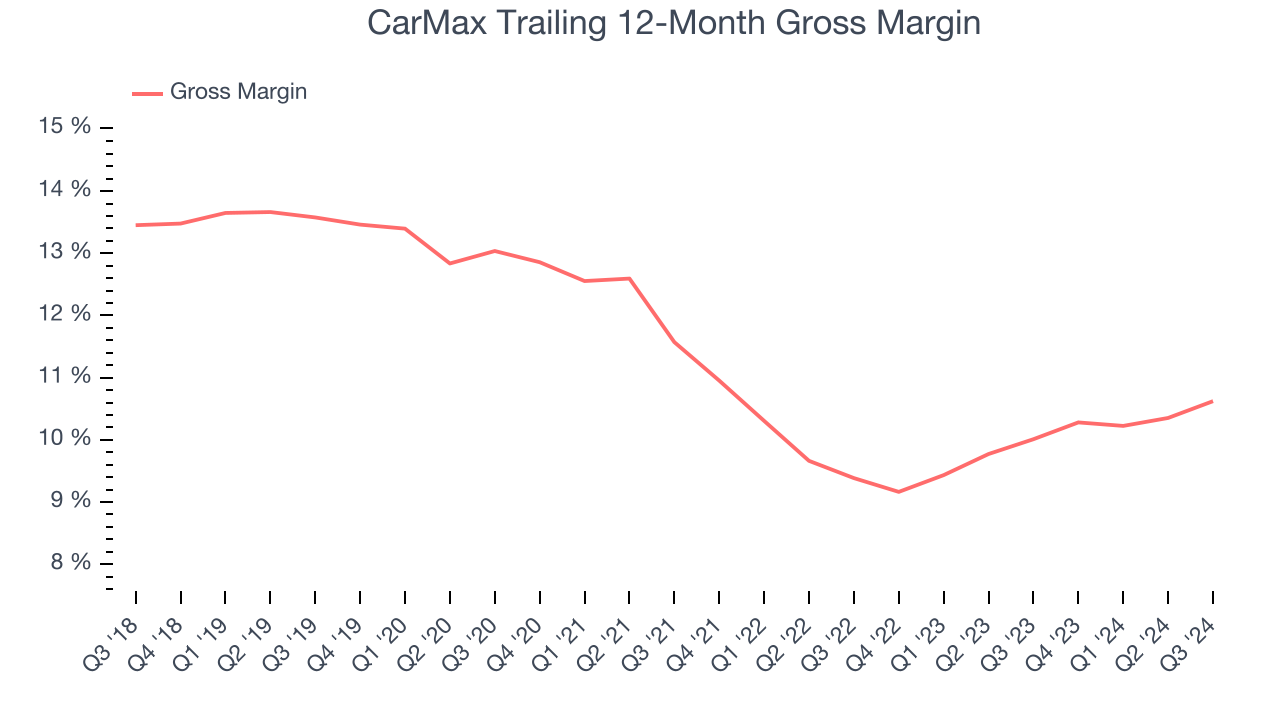

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

CarMax has poor unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 10.3% gross margin over the last two years. Said differently, CarMax had to pay a chunky $89.69 to its suppliers for every $100 in revenue.

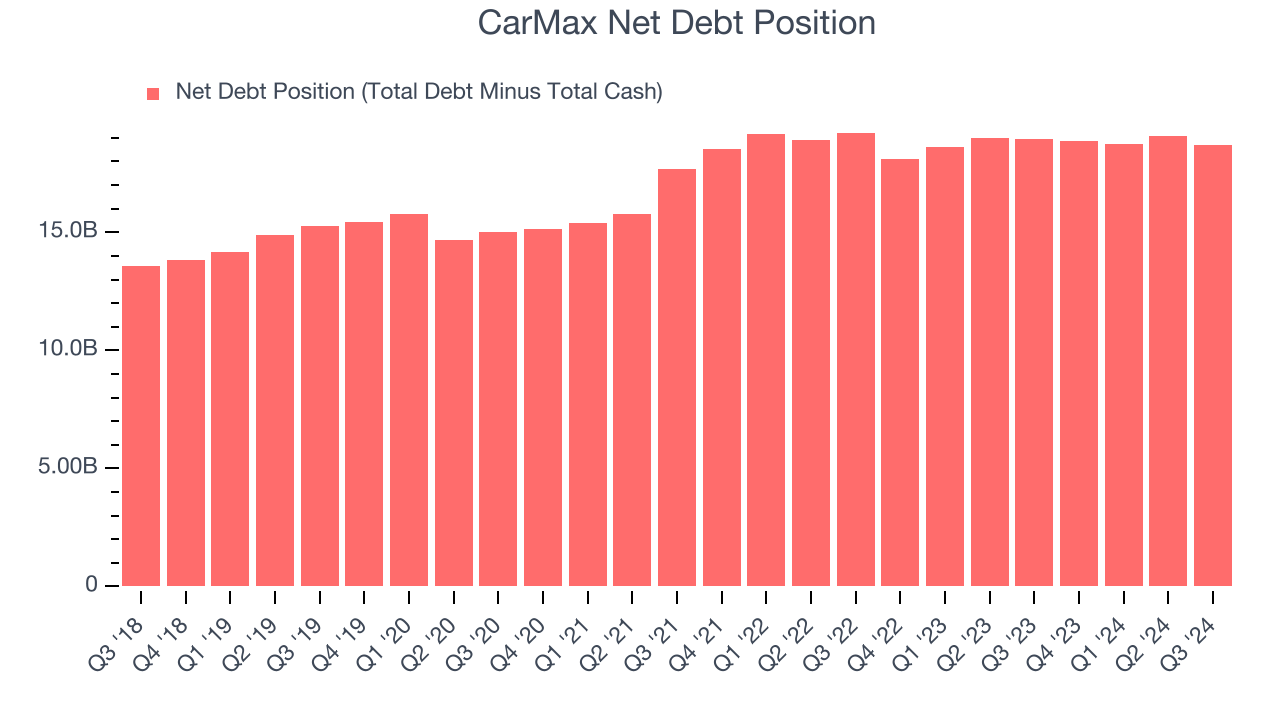

3. High Debt Levels Increase Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

CarMax’s $19.21 billion of debt exceeds the $524.7 million of cash on its balance sheet. Furthermore, its 18x net-debt-to-EBITDA ratio (based on its EBITDA of $1.02 billion over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. CarMax could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope CarMax can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

CarMax doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 24.3x forward price-to-earnings (or $85.09 per share). This valuation tells us a lot of optimism is priced in - we think there are better investment opportunities out there. Let us point you towards MercadoLibre, the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of CarMax

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.