Electronics retailer Best Buy (NYSE: BBY) fell short of the market’s revenue expectations in Q3 CY2024, with sales falling 3.2% year on year to $9.45 billion. The company’s full-year revenue guidance of $41.3 billion at the midpoint came in 0.7% below analysts’ estimates. Its non-GAAP profit of $1.26 per share was 2.5% below analysts’ consensus estimates.

Is now the time to buy Best Buy? Find out by accessing our full research report, it’s free.

Best Buy (BBY) Q3 CY2024 Highlights:

- Revenue: $9.45 billion vs analyst estimates of $9.63 billion (3.2% year-on-year decline, 2% miss)

- Adjusted EPS: $1.26 vs analyst expectations of $1.29 (2.5% miss)

- Adjusted EBITDA: $563 million vs analyst estimates of $583 million (6% margin, 3.4% miss)

- The company dropped its revenue guidance for the full year to $41.3 billion at the midpoint from $41.6 billion, a 0.7% decrease

- Management lowered its full-year Adjusted EPS guidance to $6.18 at the midpoint, a 0.8% decrease

- Operating Margin: 3.7%, in line with the same quarter last year

- Free Cash Flow was -$449 million compared to -$108 million in the same quarter last year

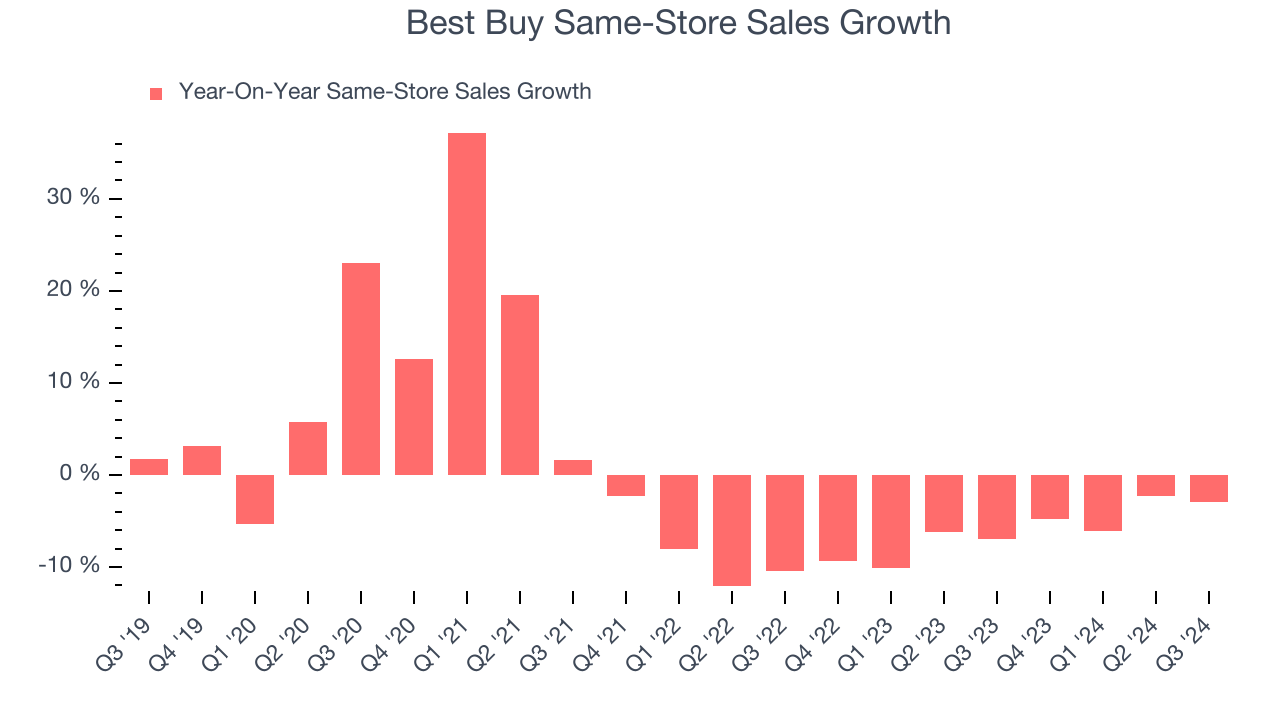

- Same-Store Sales fell 2.9% year on year (-6.9% in the same quarter last year)

- Market Capitalization: $19.98 billion

“In the third quarter, our teams delivered an in-line non-GAAP operating income rate on sales that were a little softer than expected,” said Corie Barry, Best Buy CEO.

Company Overview

With humble beginnings as a stereo equipment seller, Best Buy (NYSE: BBY) now sells a broad selection of consumer electronics, appliances, and home office products.

Electronics & Gaming Retailer

After a long day, some of us want to just watch TV, play video games, listen to music, or scroll through our phones; electronics and gaming retailers sell the technology that makes this possible, plus more. Shoppers can find everything from surround-sound speakers to gaming controllers to home appliances in their stores. Competitive prices and helpful store associates that can talk through topics like the latest technology in gaming and installation keep customers coming back. This is a category that has moved rapidly online over the last few decades, so these electronics and gaming retailers have needed to be nimble and aggressive with their e-commerce and omnichannel investments.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

Best Buy is larger than most consumer retail companies and benefits from economies of scale, enabling it to gain more leverage on fixed costs than its smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it's harder to find incremental growth when you've penetrated most of the market.

As you can see below, Best Buy struggled to increase demand as its $42.23 billion of sales for the trailing 12 months was close to its revenue five years ago (we compare to 2019 to normalize for COVID-19 impacts). This was mainly because it didn’t open many new stores and observed lower sales at existing, established locations.

This quarter, Best Buy missed Wall Street’s estimates and reported a rather uninspiring 3.2% year-on-year revenue decline, generating $9.45 billion of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and suggests its newer products will not lead to better top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Store Performance

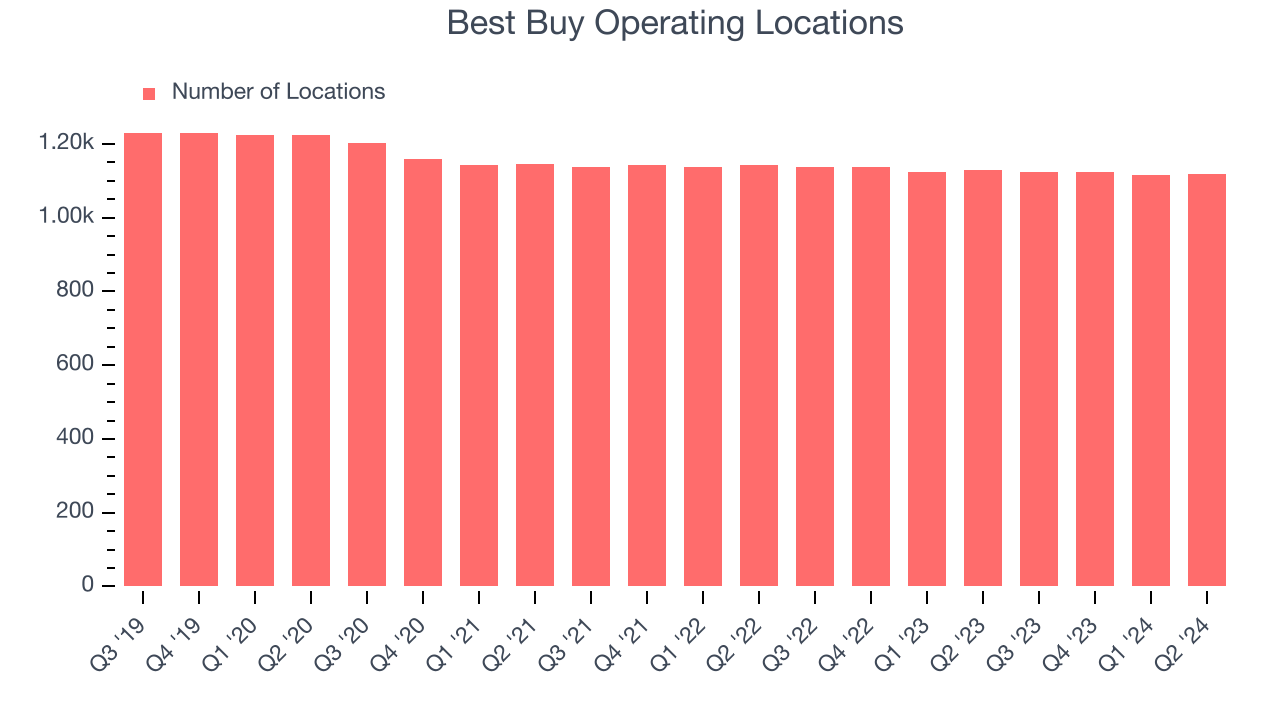

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Over the last two years, Best Buy has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Best Buy reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Best Buy’s demand has been shrinking over the last two years as its same-store sales have averaged 6.1% annual declines. This performance isn’t ideal, and we’d be concerned if Best Buy starts opening new stores to artificially boost revenue growth.

In the latest quarter, Best Buy’s same-store sales fell by 2.9% year on year. This decrease was an improvement from its historical levels. It’s always great to see a business’s demand trends improve.

Key Takeaways from Best Buy’s Q3 Results

It was tough to see Best Buy miss analysts’ revenue and EPS expectations this quarter. It also added fuel to the fire by lowering its full-year revenue and EPS guidance. Overall, this was a weaker quarter. The stock traded down 5.9% to $87.51 immediately after reporting.

Best Buy didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.