Verizon has been treading water for the past six months, recording a small return of 1.8% and holding steady at $41.22. The stock also fell short of the S&P 500 index’s 10.5% gain during that time.

Is now the time to buy Verizon, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.We're sitting this one out for now. Here are three reasons why we avoid VZ and one stock we'd rather own.

Why Do We Think Verizon Will Underperform?

Formed in 1984 as Bell Atlantic after the breakup of Bell System into seven companies, Verizon (NYSE: VZ) is a telecom giant providing a range of communications and internet services.

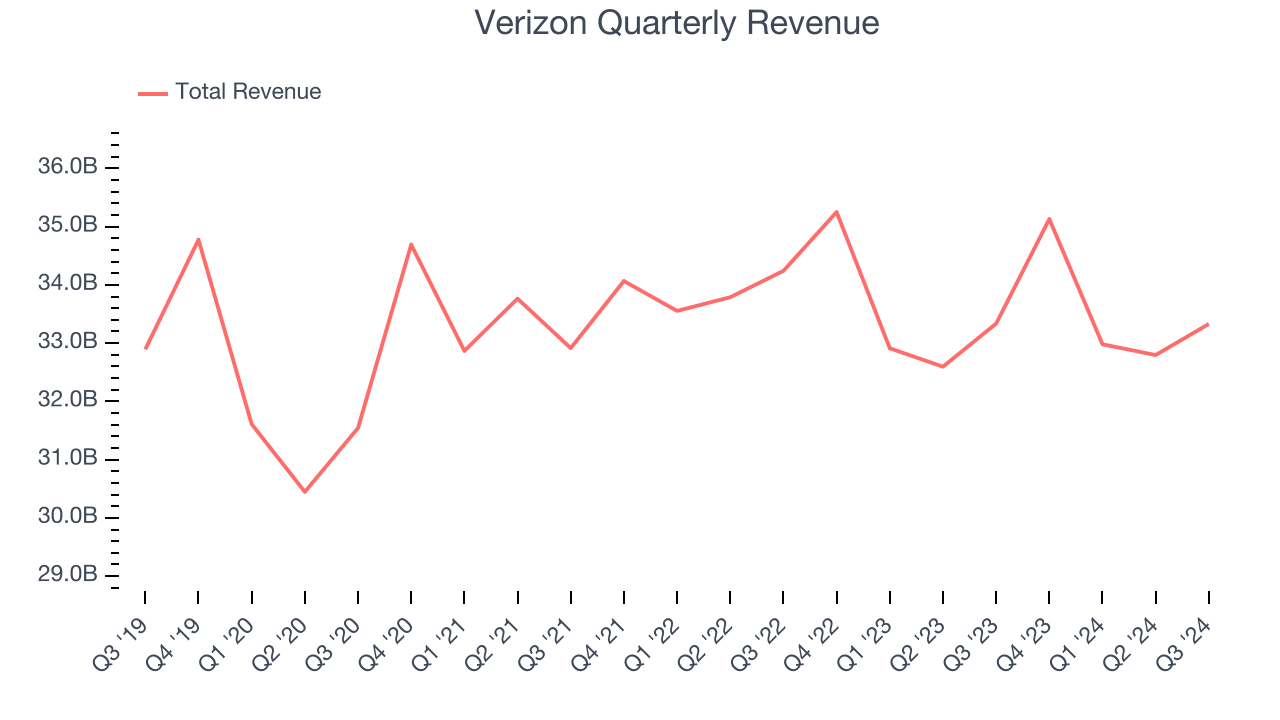

1. Long-Term Revenue Growth Flatter Than a Pancake

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one sustains growth for years. Unfortunately, Verizon struggled to increase demand as its $134.2 billion of sales for the trailing 12 months was close to its revenue five years ago.

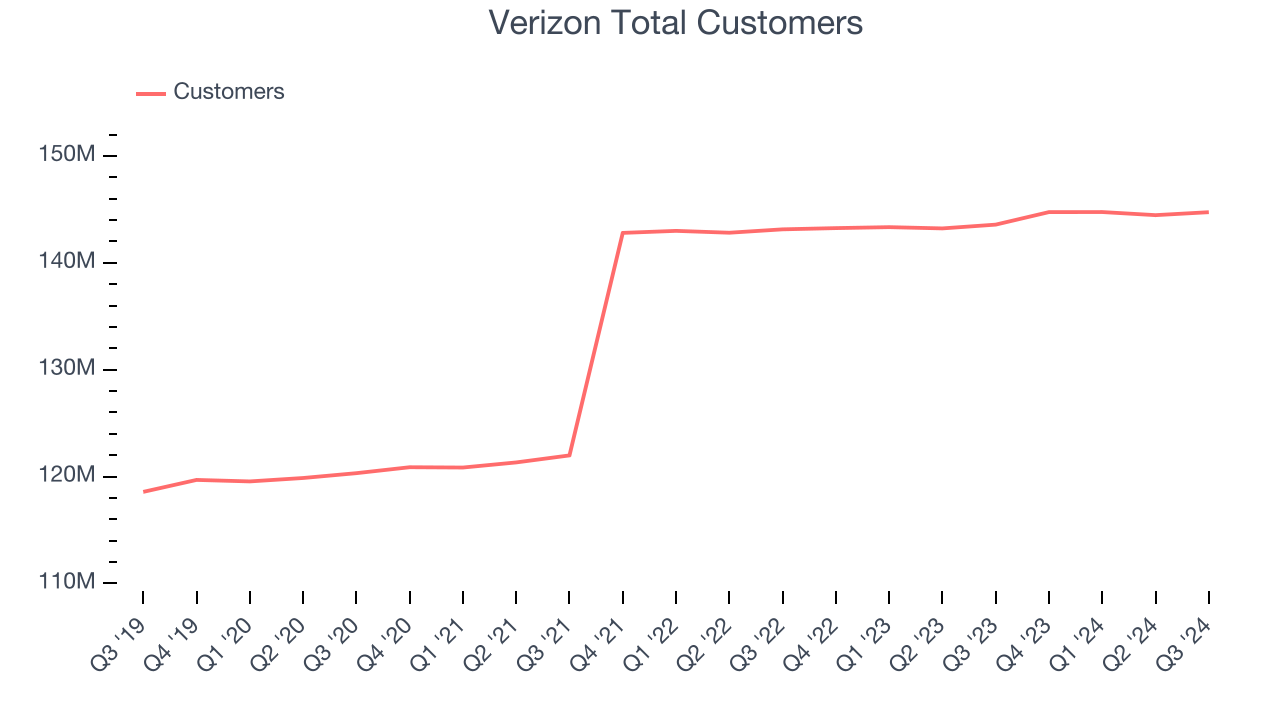

2. Customer Base Hits a Plateau

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important as an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

Over the last two years, Verizon’s total customers were flat, coming in at 144.7 million in the latest quarter. This performance was underwhelming and shows the company faced challenges in landing new contracts. It also suggests there may be increasing competition or market saturation.

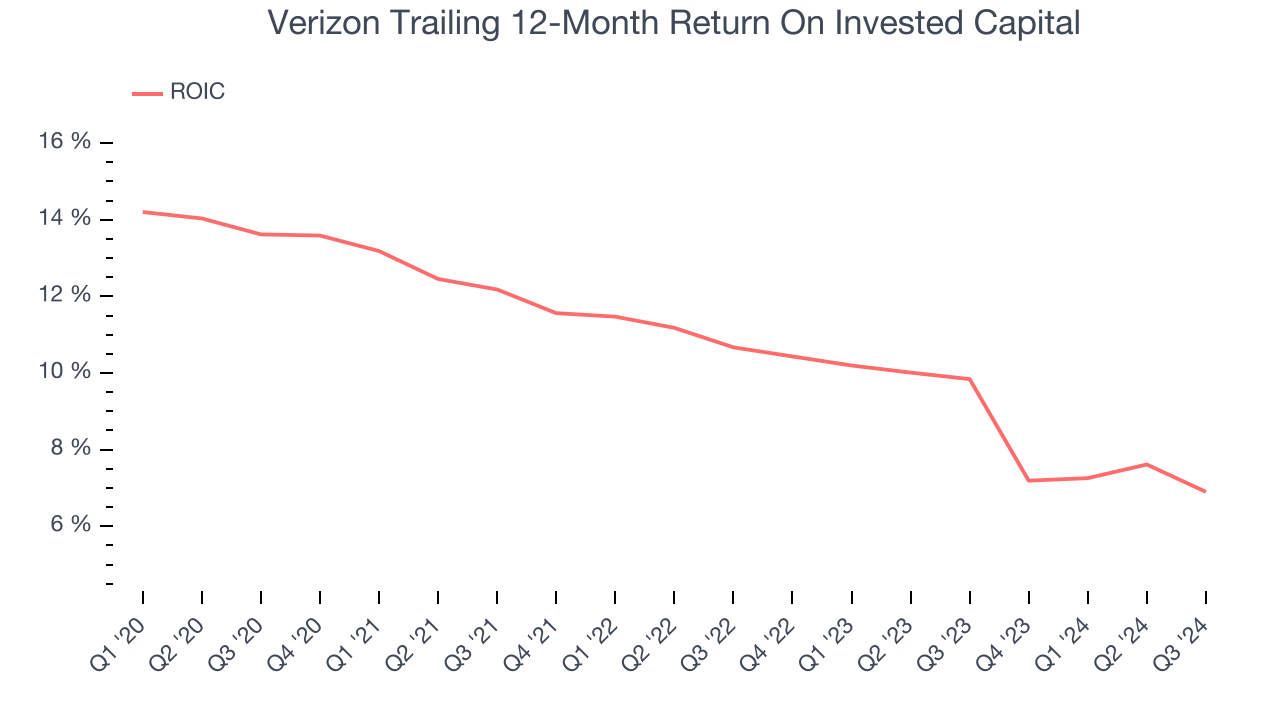

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it raised (debt and equity).

We typically prefer to invest in businesses with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. On average, Verizon’s ROIC decreased by 4.5 percentage points annually over the last few years. Paired with its already low returns, these declines suggest its profitable business opportunities are few and far between.

Final Judgment

Verizon falls short of our quality standards. With its shares underperforming the market lately, the stock trades at 8.7x forward price-to-earnings (or $41.22 per share). This valuation could be reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. We’d rather buy MercadoLibre, the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Verizon

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our High Quality Stocks with strong momentum. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.