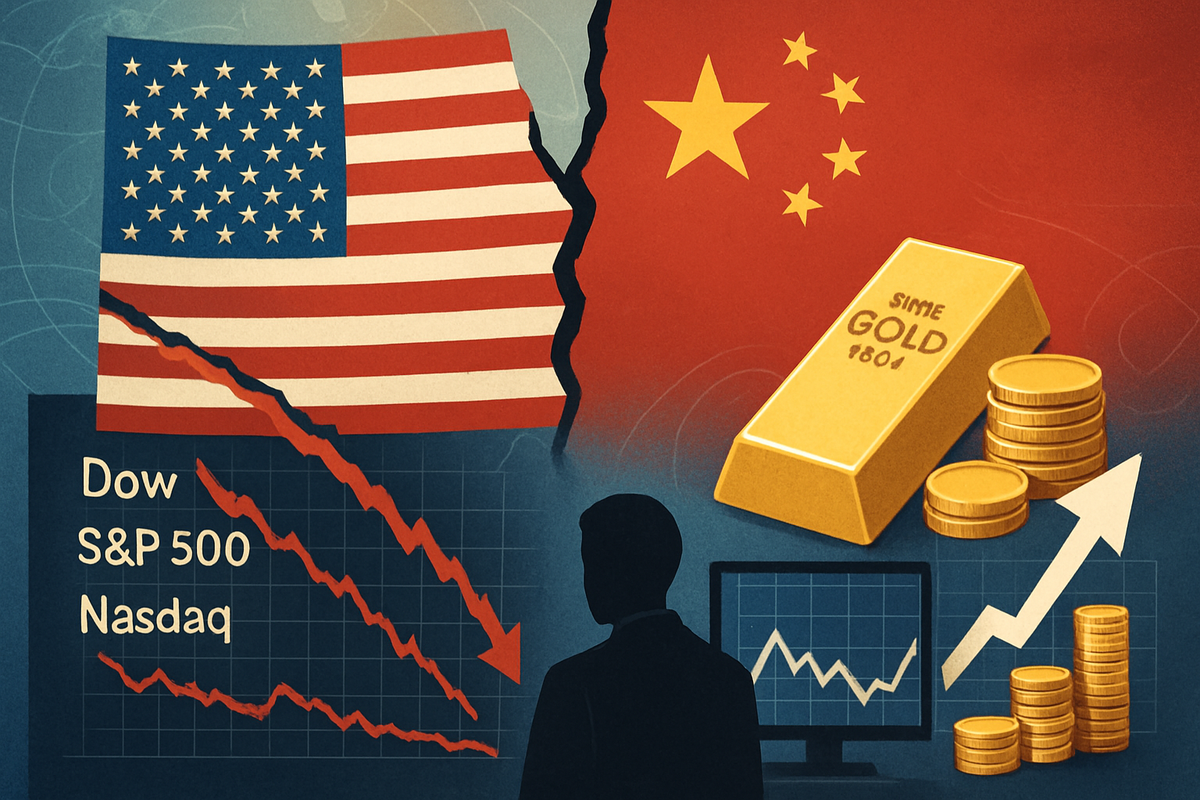

Global financial markets are once again gripped by uncertainty as a renewed trade standoff between the United States and China sends major indices spiraling into the red. In a week marked by heightened volatility, the Dow Jones Industrial Average (DJIA), S&P 500 (SPX), and Nasdaq Composite (IXIC) have all shed significant gains, reflecting deep investor apprehension. This market turmoil has concurrently propelled gold prices to unprecedented levels, with the precious metal surging past $4,200 an ounce to hit a fresh all-time high of $4,218 in the European session on October 15, 2025, as investors flock to traditional safe-haven assets amidst the escalating geopolitical friction.

This sudden downturn, characterized by sharp daily declines and a pervasive sense of caution, underscores the fragility of the global economic recovery and the profound impact that US-China relations continue to exert on financial stability worldwide. The immediate implications include a widespread flight from risk assets, a strengthening of defensive currencies, and a palpable fear of broader economic repercussions, reminiscent of past trade disputes but with potentially more severe consequences given the current global economic landscape.

Escalating Tensions Drive Market Sell-Off and Gold Rush

The current market instability stems directly from a significant escalation in the ongoing trade dispute between the United States and China, which flared up dramatically in early October 2025. On October 10, the S&P 500 (SPX) plummeted 2.7%, marking its steepest single-day drop since April, contributing to a 2.4% weekly decline, while the Nasdaq Composite (IXIC) tumbled 3.6%. The Dow Jones Industrial Average (DJIA) also shed 879 points, or 1.8%, on that day. The selling pressure continued, with the Dow falling over 500 points (1.1%) on October 14, the S&P 500 (SPX) losing 1.3%, and the Nasdaq Composite (IXIC) sliding nearly 2%.

This latest chapter in the trade standoff has seen both nations announce new retaliatory measures and threats, triggering a domino effect across global bourses. The Cboe Volatility Index (VIX), often dubbed Wall Street's "fear gauge," surged above its long-term average, reaching as high as 22.76 on October 14, its highest intraday level since May 23. Technology and semiconductor companies, particularly those with substantial exposure to the Chinese market, bore the brunt of the sell-off. Simultaneously, gold, a traditional safe haven, saw an extraordinary rally. After hitting $3,177.5 in April 2025, spot gold prices jumped above $4,100 earlier in October, culminating in a new all-time high of $4,218 an ounce on October 15. This surge is largely attributed to a weakening US dollar and the intensifying trade fears, driving investors to the perceived safety of the precious metal.

The timeline of events leading to this moment is characterized by a series of tit-for-tat actions. While the US-China trade war has simmered since January 2018, with a "phase one" agreement in 2020 doing little to dismantle existing tariffs, recent weeks have seen a dramatic intensification. Public statements from both Washington and Beijing have injected significant policy uncertainty into the markets, a factor deeply unsettling to investors. This "back-and-forth rhetoric" has fueled rapidly shifting sentiment, with brief market rebounds quickly giving way to renewed selling pressure as new threats or retaliatory measures emerge. Beyond stocks and gold, the US dollar has weakened against defensive currencies like the Japanese Yen and Swiss Franc, while oil prices have fallen by more than 1% on fears of diminished global demand, and global bonds have rallied as investors pull back from risk.

Companies Navigating the Trade War Minefield

The renewed US-China trade standoff creates a clear divide between potential winners and losers in the corporate landscape, particularly for publicly traded companies. Companies with extensive supply chains in China or significant revenue exposure to the Chinese consumer market are likely to face substantial headwinds. Technology giants such as Apple (NASDAQ: AAPL), which relies heavily on Chinese manufacturing and sales, could see disruptions in production and a hit to their bottom line from tariffs and reduced consumer demand. Similarly, semiconductor companies like Qualcomm (NASDAQ: QCOM) and NVIDIA (NASDAQ: NVDA), whose components are crucial for Chinese tech products, face the dual threat of supply chain disruptions and diminished orders from their largest market. Retailers and consumer goods companies that import heavily from China, such as Walmart (NYSE: WMT) and Nike (NYSE: NKE), may be forced to absorb higher costs or pass them on to consumers, potentially impacting sales and profit margins.

Conversely, companies with a more localized supply chain or those that benefit from a flight to quality could emerge as relative winners. Domestic manufacturing companies that can capitalize on "reshoring" trends, though a long-term prospect, might see increased demand. Companies in the defense sector or those providing essential services with minimal international trade exposure could also be more resilient. The most significant beneficiaries, however, are likely to be found in the commodities sector, particularly gold miners. Companies like Newmont Corporation (NYSE: NEM) and Barrick Gold Corporation (NYSE: GOLD) are poised to see increased revenues and profitability as the price of gold continues its ascent. Their stock prices typically correlate positively with gold prices, offering a hedge against broader market downturns driven by geopolitical tensions.

Furthermore, companies involved in cybersecurity or strategic national infrastructure, which become priorities during periods of geopolitical tension, might see sustained government contracts. Pharmaceutical companies with diversified global operations might also be less susceptible to direct trade tariff impacts, though broader economic slowdowns could still affect them. The key for companies in this environment is agility: those capable of quickly reconfiguring supply chains, diversifying their market reach, or innovating to reduce reliance on specific geopolitical regions will be better positioned to weather the storm. The trade standoff is compelling many multinational corporations to reassess their global strategies, potentially leading to long-term shifts in production and market focus.

Broader Implications and Historical Parallels

This latest escalation in the US-China trade standoff is more than just a momentary market blip; it fits into a broader, more concerning trend of deglobalization and geopolitical fragmentation. The push for economic decoupling, driven by national security concerns and a desire for supply chain resilience, has been gaining momentum for years. This event underscores the increasing weaponization of trade and technology, transforming economic interdependence into a source of vulnerability. The potential ripple effects are vast, extending beyond direct trade partners. Competitors in other emerging markets may see opportunities to attract manufacturing or investment diverted from China, while partners dependent on global trade stability, such as European and East Asian economies, face significant collateral damage.

Regulatory and policy implications are profound. Governments on both sides are likely to double down on protectionist measures, potentially leading to a more fractured global trading system. This could manifest in increased scrutiny of foreign investments, stricter export controls, and greater emphasis on domestic industrial policies. The International Monetary Fund (IMF) has repeatedly warned that sustained trade fragmentation could erode global GDP by up to 7% over time, highlighting the severe long-term economic costs. There's also the risk of a "COVID-like shock" to the US economy if China were to restrict exports of rare earth minerals, crucial for high-tech industries, leading to a significant slowdown in GDP growth and a surge in wholesale inflation.

Historically, periods of intense trade friction, such as the Smoot-Hawley Tariff Act of 1930, have demonstrated the devastating consequences of protectionism, contributing to the Great Depression. While the current situation is different, the underlying principle remains: trade wars are rarely beneficial for any party involved. More recently, the initial phases of the US-China trade war from 2018-2019 also saw similar patterns of market volatility, investor uncertainty, and a flight to safe-haven assets like gold. This current escalation, however, appears to be occurring within an already fragile global economic environment, potentially amplifying its negative impact and making a swift resolution more challenging. The imposition of new port fees by both nations on each other's vessels further signals a deepening of the conflict, directly impacting the logistics that underpin over 80% of international trade.

What Comes Next: A Path Forward Amidst Uncertainty

The immediate future for global markets hinges precariously on the trajectory of the US-China trade standoff. In the short term, investors should brace for continued volatility, with market sentiment likely swinging wildly based on every new statement or action from Washington and Beijing. The "buy-the-dip" enthusiasm that characterized previous market corrections appears to be fading, replaced by a more cautious approach. Companies will need to prioritize supply chain resilience, exploring diversification strategies away from over-reliance on single regions. This could mean increased investment in automation, domestic production, or establishing manufacturing hubs in other friendly nations. For investors, the appeal of safe-haven assets like gold is expected to persist, potentially pushing prices even higher, while defensive sectors and companies with strong balance sheets may offer some refuge.

Looking further ahead, the long-term possibilities are more complex and could range from a negotiated de-escalation to a more entrenched economic cold war. A "phase two" trade deal, while elusive, remains a possibility that could provide a significant boost to market confidence. However, if the current trajectory continues, we could see a more permanent restructuring of global supply chains and trade relationships. This scenario would present both challenges and opportunities: challenges for multinational corporations adapted to a globalized world, and opportunities for nations and companies that can strategically position themselves within new, potentially bifurcated, economic blocs. Market opportunities may emerge in sectors focused on domestic infrastructure, renewable energy (to reduce geopolitical energy dependencies), and advanced manufacturing as nations seek greater self-sufficiency.

Potential scenarios include a rapid resolution driven by economic pressures on both sides, a prolonged period of low-intensity conflict marked by sporadic escalations, or a full-blown economic decoupling. The latter could lead to significant global economic restructuring, with implications for everything from technology standards to international finance. Investors should closely monitor diplomatic efforts, any shifts in rhetoric, and economic data (especially inflation and GDP growth figures) for clues about the direction of the conflict. The ability of central banks to mitigate economic fallout with monetary policy will also be a critical factor to watch, though their tools may be limited in addressing fundamental trade imbalances.

A Turbulent Outlook: Assessing the Lasting Impact

The current market turbulence, driven by the escalating US-China trade standoff and the subsequent surge in gold prices, serves as a stark reminder of the interconnectedness of global finance and geopolitics. The key takeaway from this event is the profound uncertainty it injects into the global economic outlook. Investor sentiment has shifted decidedly towards caution, with a clear flight to safety, highlighting the market's deep apprehension about the potential for a prolonged trade war to derail economic recoveries and inflict significant damage. The record-breaking performance of gold underscores the severity of this fear, as investors seek tangible assets to protect against currency depreciation and economic instability.

Moving forward, the market will remain highly sensitive to any developments in US-China relations. The "new normal" may involve higher levels of volatility and a sustained demand for assets perceived as safe. Companies must critically assess their supply chain vulnerabilities and market dependencies, with strategic pivots towards diversification and localization becoming imperative. The lasting impact of this period could be a more fragmented global economy, characterized by regional trade blocs and increased protectionism, rather than the free-flowing globalized system of previous decades. This shift will necessitate fundamental changes in corporate strategy, government policy, and investment approaches.

Investors should continue to watch for several key indicators in the coming months: any progress or further deterioration in trade negotiations, the trajectory of inflation and global GDP growth, and the policy responses from major central banks. The performance of key sectors, particularly technology and manufacturing, will offer insights into the real-world impact of the trade war on corporate earnings. Ultimately, this trade standoff is more than just a temporary market correction; it represents a significant challenge to the existing world order, with long-term implications for global economic stability and the future of international commerce.

This content is intended for informational purposes only and is not financial advice