Chewy’s (NYSE: CHWY) stock price dipped following the FQ3 2025 earnings report, which opened a buy-the-dip opportunity. The results were mixed relative to the analysts' expectations but aligned with pet industry trends and an outlook for sustained growth. The trends include another quarter of declining active users compared to the previous year but suggest active users will revert to growth soon and maintain growth over the next few years.

The primary cause for user count declines is post-pandemic normalization, which has just about run its course. The decline in Q3 is only 0.5% and is offset by other metrics that show leverage building for when macroeconomic headwinds ease. That is expected in 2025 as interest rates fall and Trump’s economic policies begin to take effect. Critical details within the report include the sequential improvement in user count, increasing revenue per user, and the high 77% recurring revenue rate. Autoship metrics indicate that the recurring revenue is visible and growing, providing a solid foundation from which growth can accelerate for the eCommerce retailer when the user count metrics improve and macroeconomic headwinds ease.

Chewy Falls After Missing the Analysts' High Expectations

Chewy's quarter was mixed relative to the analysts' consensus forecast reported by MarketBeat. Still, it was a solid quarter, growing in alignment with industry trends as economic headwinds offset market share gains. The company reported $2.88 billion in net revenue for a gain of 4.8% over last year, outpacing the consensus estimate by nearly 100 basis points. The strength was driven by a 4.2% increase in revenue per user, offset by a slight 0.5% decline in active users. Autoship sales grew by 8.7% and are expected to continue leading the business in 2025.

The margin news is good despite the earnings falling short of the consensus. The company widened its margin at the gross and operating levels, produced GAAP profits, and grew adjusted EPS by 33%. The $0.20 in adjusted EPS fell short of the consensus by $0.03, but the revisions set the bar high, and the miss is offset by guidance. Chewy raised guidance for Q4 and the full year to levels above the consensus estimate, sufficient to sustain the analysts' sentiment if not lead to improvement.

The analysts' sentiment trends are positive at the end of 2024 after reverting from negative earlier in the year. The consensus target increased nearly 1500 basis points since early fall, leading the market to the high-end range near $40. A move to consensus is worth 7.5% of the critical support target, and a move to the high-end range is closer to 32.5% of the critical support.

Institutional Activity May Cap Gains in Chewy Stock

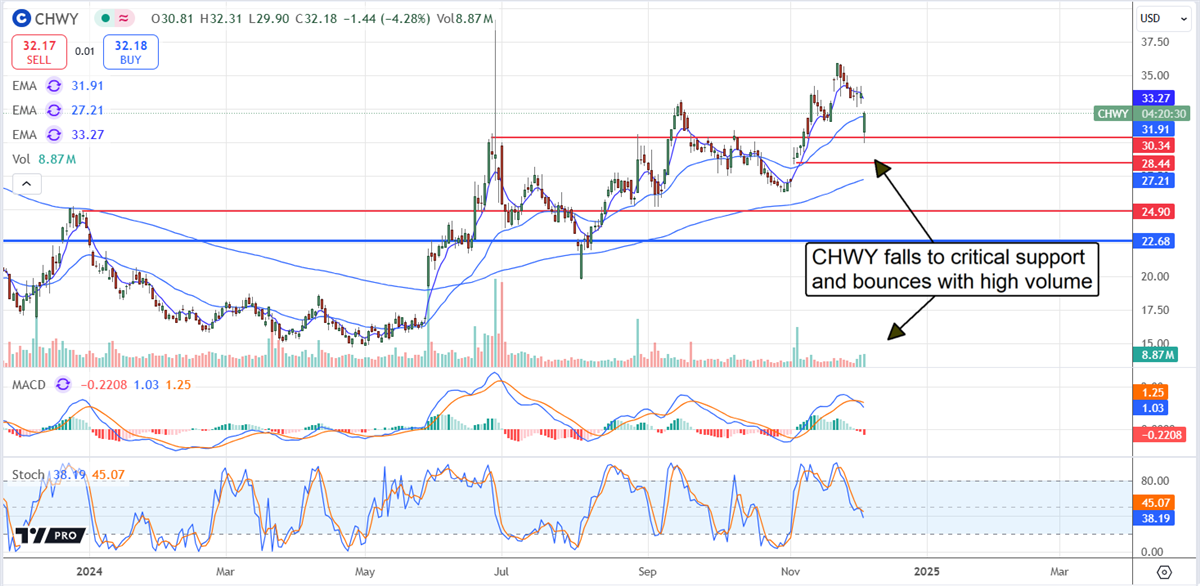

The institutional activity in Q4 is bearish for CHWY stock and may cap gains when the share price advances. However, the activity in 2024 is bullish on balance and aligns with the market uptrend that began in May. The pullback in share prices creates an opportunity for the group and retail investors; the question is if they will resume the buying activity. If so, CHWY stock price should begin to rebound soon. If not, it could fall below critical support targets near $30.50.

The price action gives reason for optimism. The market fell in reaction to the news but bounced off of the critical support target and showed signs of rebounding. Signs of rebounding include the increased volume, which doubled the daily average in the first two hours of trading. The uptrend in the stock price should continue, assuming support holds at $30.50. If not, this stock could fall to $28.50 or lower before hitting a solid bottom.