Apple (AAPL) builds consumer tech that blends hardware, software, and services into one seamless experience, keeping users deeply connected within its ecosystem. Over time, it has turned that integration into a powerful revenue engine, driving both device sales and recurring income.

Now, after years of silence in its premium headphone lineup, Apple is back with a fresh update that’s already catching the market’s attention. The company has unveiled the AirPods Max 2, its first major refresh since 2020, giving AAPL stock a slight lift.

At $549, Apple clearly is not trying to play the budget game. Instead, it is leaning deeper into the premium space, packing in its H2 chip, better noise cancellation, improved mic quality, and a bunch of artificial intelligence (AI)-driven features like Live Translation and Adaptive Audio. It is the kind of upgrade that feels smooth and polished. In other words, very on brand for Apple.

But zooming out a bit, this launch is about more than just headphones. Apple is up against strong rivals like Sony Group (SONY) and Bose Corporation, all fighting for the same high-end customer.

Sure, it’s a solid upgrade, but is it enough to really move the needle for Apple’s stock story, especially when AAPL is already in the red in 2026?

About Apple Stock

Apple, the $3.7 trillion technology giant born in Cupertino, California, has spent decades reshaping how the world works, creates, and connects. From the iPhone that redefined mobility to the Mac and iPad that blurred the line between work and creativity, Apple built its reputation on products that feel personal yet powerful.

Today, its story has evolved beyond devices. The company’s growing services business has become a quiet force, anchored by more than a billion paid subscriptions. High-margin offerings like iCloud, Apple Music, and the App Store now form a steady backbone, helping Apple navigate global uncertainty while deepening user loyalty.

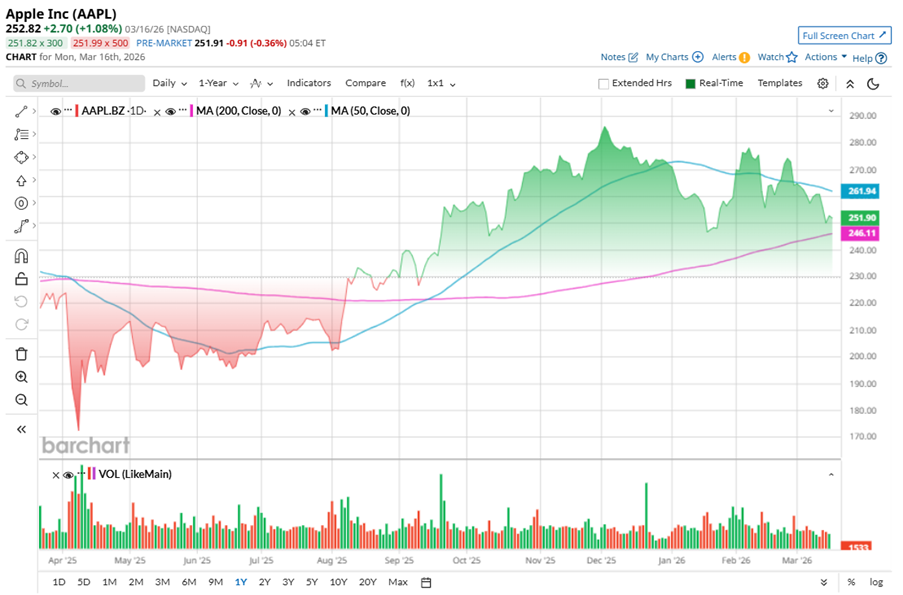

Apple might still wear the innovation crown, but its stock chart this year tells a slightly more complicated story. AAPL has not exactly had a smooth ride, caught in a mix of global tensions and shifting tech sentiment. With uncertainty around geopolitical issues like the U.S.-Iran war and growing whispers of an AI bubble, risk appetite has taken a hit.

Tech stocks have felt the pressure, and Apple has not been immune. The stock is down 6.54% year-to-date (YTD) and has slipped nearly 2.59% over the past five days alone.

But zoom into the chart, and it’s more of a story than a straight fall. After dipping into the $200 zone in early August, Apple staged a steady, disciplined recovery. Momentum pushed it all the way to a peak of $288.62 in early December. Since then, though, profit-booking has kicked in, pulling the stock back toward the $250 range. It’s now in correction territory, down roughly 9.4% from its YTD highs of $280.90.

Yet, despite the recent pullback, Apple is up 18.73% over the past 52 weeks, showing that even through volatility, it tends to find its footing again.

From a technical lens, signals are mixed. Trading above its 200-day moving average suggests the long-term trend is still intact, but slipping below the 50-day moving average points to near-term weakness and cautious sentiment.

Apple’s valuation is not cheap. Priced at roughly 29.74 times forward adjusted earnings and about 7.98 times sales, AAPL is clearly sitting in premium territory. But for Apple, that price tag reflects strength, not hype. Investors are paying for a sticky ecosystem, unmatched brand loyalty, and a business that delivers steady results at scale.

That confidence shows up in returns, too. Apple has raised its dividend for 13 consecutive years, yet pays out only about 13% of its profits. That leaves plenty of room to grow payouts ahead, quietly reinforcing why investors are willing to pay up.

A Snapshot of Apple’s Q1 Results

Apple walked into 2026 with serious momentum, and its fiscal first-quarter results, released on Jan. 29, made that pretty clear. The company delivered a record performance, raking in massive revenue of $143.8 billion, up 16% year-over-over (YOY), while EPS rose 19% annually to $2.84, comfortably beating Wall Street’s expectations.

The real engine behind this growth was the iPhone. The segment pulled in $85.3 billion in revenue, a sharp 23.3% annual jump, as demand for the latest lineup stayed strong across markets. At the same time, Apple’s services business continued to quietly shine, bringing in a record $30 billion in revenue, up 14%. This part of the business, with its high margins, is steadily becoming Apple’s backbone.

Not everything was impressive, though. iPad revenue saw a modest rise to $8.6 billion, while Mac revenue dipped to around $8.4 billion, reflecting softer demand in the broader PC market. Wearables, Home, and Accessories brought in $11.5 billion, slightly down from last year.

One might think that a quarter like this would spark a rally in AAPL stock, but it barely blinked. That is because the focus quickly shifted from what went right to what could go wrong for Apple next.

Ironically, demand is part of the problem. The latest iPhones sold so well that Apple ended the quarter with tighter-than-usual inventory. And with supply chains still not fully flexible, that could limit how much the company can capitalize on that demand in the coming months. At the same time, costs are starting to creep in. Memory prices didn’t hurt much in the December quarter, but Apple expects a bigger impact ahead, with prices continuing to rise. That could put some pressure on margins if the trend sticks.

Even so, overall, the management seemed confident. The revenue growth is guided between 13% and 16% in the March quarter, suggesting the momentum is not fading anytime soon. And, margins are expected to hold up, supported by a strong product mix.

Beyond the short-term noise, Apple’s expanding ecosystem and high-margin services business continue to act as a strong backbone for growth.

Analysts monitoring the company remain optimistic, predicting EPS to be around $8.41 for fiscal 2026, up 12.73% YOY, before surging another 10.46% annually to $9.29 in fiscal 2027.

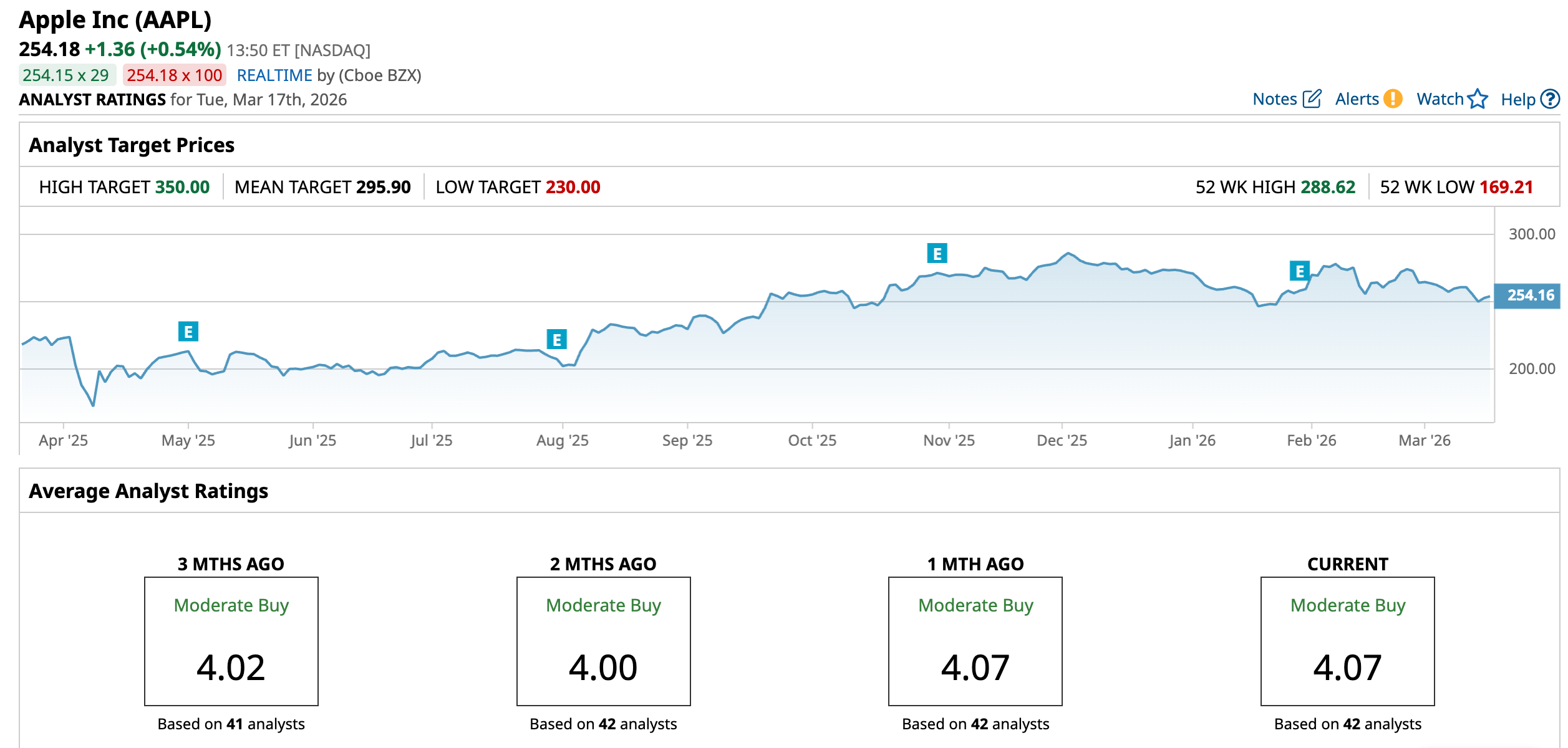

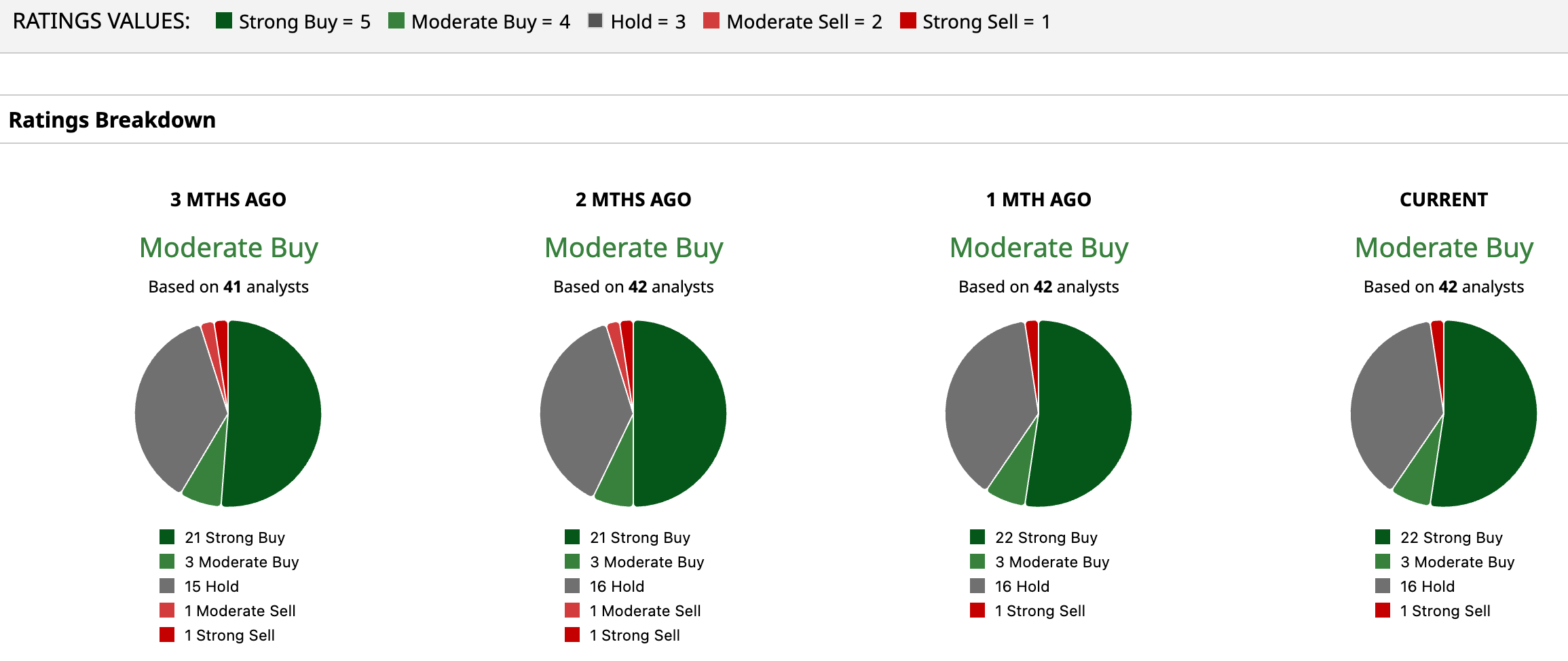

What Do Analysts Expect for Apple Stock?

AAPL stock has a consensus “Moderate Buy” rating overall. Out of 42 analysts covering the tech stock, 22 recommend a “Strong Buy,” three give a “Moderate Buy,” 16 analysts stay cautious with a “Hold” rating, and the remaining one analyst has a “Strong Sell” rating.

The average analyst price target for AAPL is $295.90, indicating potential upside of around 16.4% from here. However, the Street-high target price of $350 suggests that the stock could rally as much as 37.7%.

Final Thoughts on AAPL Stock

The AirPods Max 2 looks like a nice upgrade, but not something that will dramatically change the stock’s direction on its own. Apple’s real strength still comes from its iPhones, growing services business, and the tight ecosystem it has built over time.

Yes, there are short-term worries like the supply issues, rising costs, and a slightly shaky tech environment, but those feel more like speed bumps than roadblocks. Analysts are still largely positive, with expectations of steady growth and decent upside from here.

So, while the stock may look a bit slow right now, the bigger picture still indicates that Apple has the engine, and it just needs time to pick up speed again.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart