Fresh controversy has once again pulled Intel Corporation (INTC) into the spotlight. On March 12, INTC stock slid 5.7% after news broke that a shareholder had filed a lawsuit accusing the company of handing the U.S. government a 10% equity stake largely to shield itself from political pressure linked to the administration of Donald Trump.

The complaint, lodged in the Delaware Court of Chancery by shareholder Richard Paisner, characterizes the arrangement as an “unlawful contract that gives the U.S. government $11B worth of Intel stock for no meaningful consideration in response to extortionary threats by the government.”

Paisner contends that Intel’s board breached its fiduciary duties by approving the stake under pressure stemming from Trump’s online attacks and now seeks to have the agreement voided. The lawsuit also names the U.S. Department of Commerce and Commerce Secretary Howard Lutnick as defendants, along with Intel board chair Frank Yeary, who stepped down earlier this month.

With legal risks entering the equation just as Intel works to rebuild momentum, let us see whether INTC stock still deserves a place in portfolios.

About Intel Stock

Headquartered in Santa Clara, California, Intel designs and manufactures semiconductors that power personal computers, data centers, and the rapidly expanding artificial intelligence (AI) infrastructure ecosystem. With a market cap of roughly $226 billion, the company produces CPUs, GPUs, networking chips, and advanced fabrication services.

Despite recent short-term volatility, Intel’s longer-term price trajectory still tells a stronger story. Over the past three months, the stock has climbed 20.69%. The six-month view paints an even brighter picture, with shares surging 89.5%. Stepping back further, the stock has advanced 92.54% over the last 52 weeks.

However, from a valuation standpoint, investors now pay a premium for that progress. INTC stock is currently trading at 93.68 times forward-adjusted earnings and 4.20 times sales. Both multiples sit above industry averages and Intel’s own five-year valuation range.

Intel Surpasses Q4 Earnings

On Jan. 22, Intel released its fourth-quarter fiscal 2025 results, wherein revenue declined 4.1% year-over-year (YOY) to $13.67 billion, yet comfortably exceeded analyst estimates of $13.37 billion.

Profitability also moved in the right direction. Non-GAAP net income increased 35% to $767 million compared with the prior year’s quarter. Meanwhile, adjusted EPS grew 15.4% from the year-ago value to $0.15, beating the Street’s expectations of $0.08.

Even so, the stock lost some steam after management issued softer guidance for the upcoming quarter. Intel expects first-quarter fiscal 2026 revenue between $11.7 billion and $12.7 billion with breakeven adjusted EPS. The outlook fell short of analyst estimates, who had projected $0.05 in EPS on $12.51 billion in sales. Management attributed part of the weaker outlook to supply limitations tied to seasonal demand.

However, the company highlighted a technological milestone that could shape its longer-term trajectory. The rollout of Intel’s first products built on the Intel 18A process, the most advanced semiconductor manufacturing technology developed and produced in the U.S., marks a significant step forward.

Looking ahead, analysts expect volatility before a more meaningful earnings recovery. Forecasts call for Q1 fiscal 2026 EPS to decline 450% YOY to $0.11. But, for the full fiscal year 2026, analysts expect the bottom line to climb 150% to $0.06. By fiscal 2027, projections point to a far stronger rebound, with earnings expected to rise another 800% to $0.54.

What Do Analysts Expect for Intel Stock?

Wall Street remains cautious but not pessimistic. At KeyBanc Capital Markets, analyst John Vinh maintains an “Overweight” rating on INTC stock and recently lifted his price target from $60 to $65.

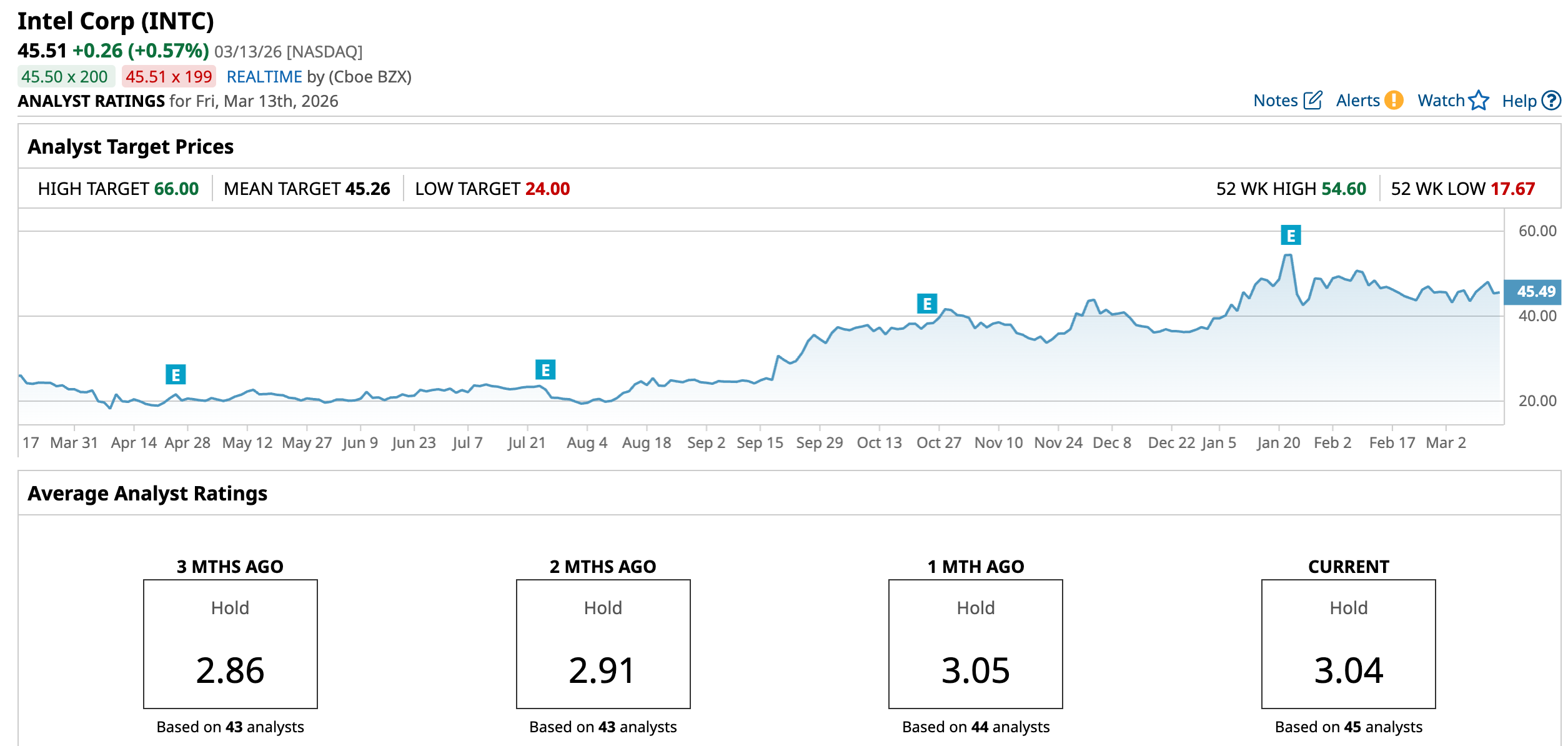

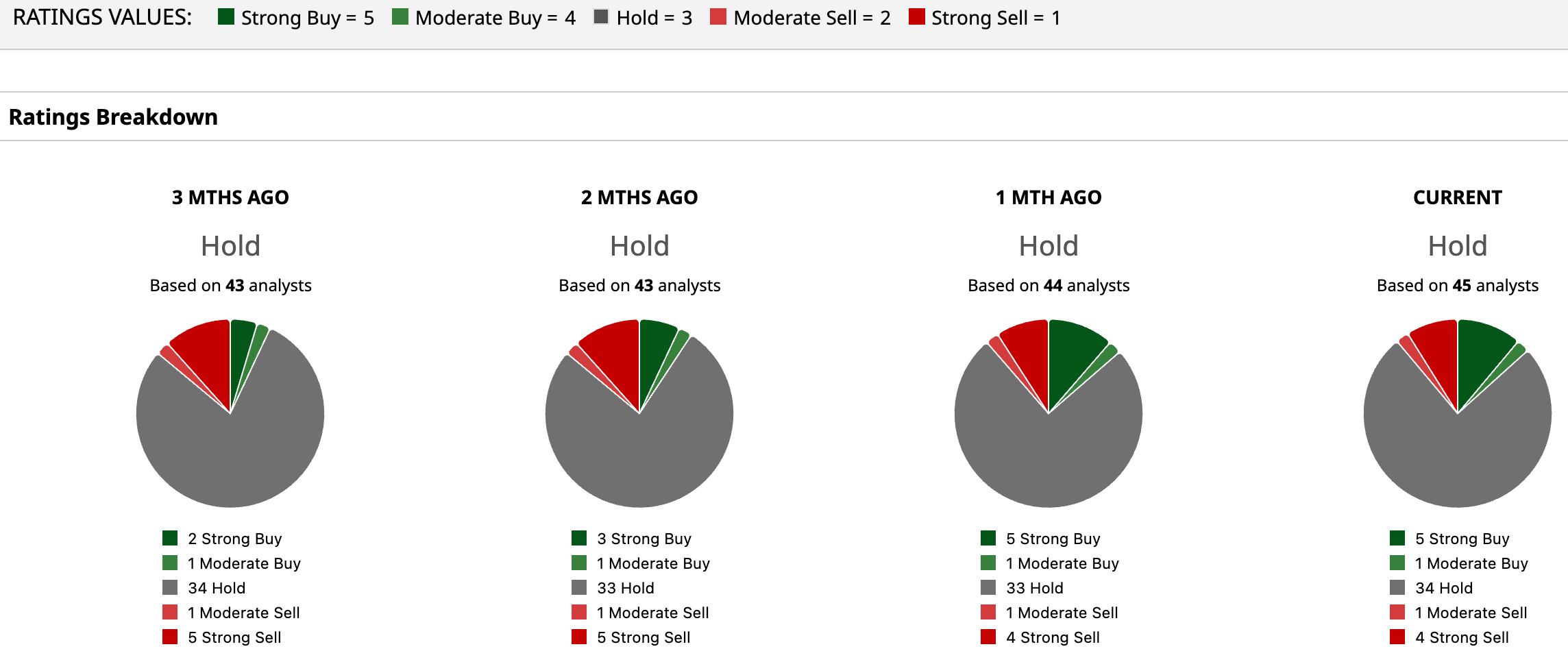

Across the broader analyst community, the consensus stance lands squarely in the middle with an overall rating of “Hold”. Among 45 analysts covering the stock, five recommend “Strong Buy,” one suggests “Moderate Buy,” and 34 advise “Hold.” One analyst flags a “Moderate Sell,” while four maintain “Strong Sell” ratings.

Nevertheless, the stock is trading slightly beyone its average price target of $45.26. Meanwhile, the Street-high target of $66 suggests a gain of 45% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy the Dip in Adobe Stock Today?

- Microsoft Is Racing to Beat Claude Cowork. A Big Catalyst for MSFT Stock Is Coming May 1.

- As a Shareholder Sues Intel for Trump Deal, Should You Be Buying, Selling, or Holding INTC Stock?

- IonQ Just Secured a Deal with the University of Cambridge. Should You Buy the Quantum Computing Stock Here?