Over the past six months, Domino’s shares (currently trading at $376.54) have posted a disappointing 12.2% loss, well below the S&P 500’s 1.1% gain. This may have investors wondering how to approach the situation.

Given the weaker price action, is now a good time to buy DPZ? Find out in our full research report, it’s free.

Why Does DPZ Stock Spark Debate?

Founded by two brothers in Michigan, Domino’s (NYSE: DPZ) is a globally recognized pizza chain known for its creative marketing and fast delivery.

Two Positive Attributes:

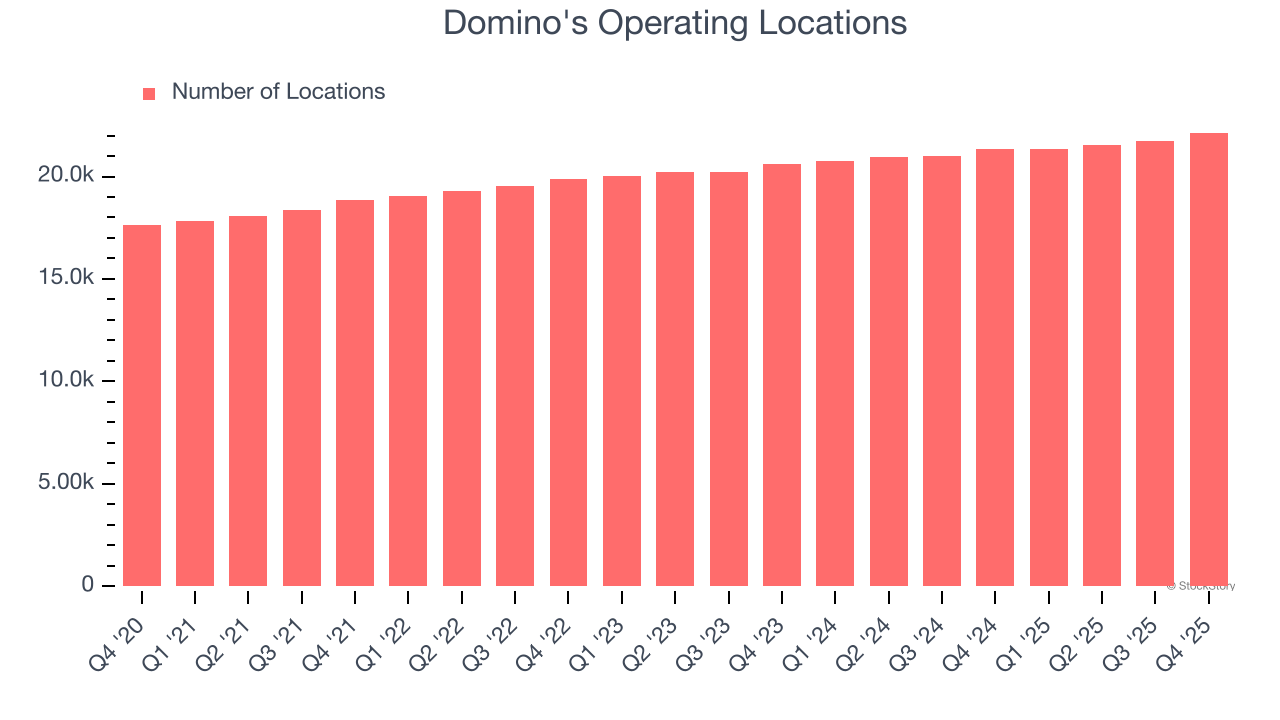

1. Restaurant Growth Signals an Offensive Strategy

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Domino's sported 22,142 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 3.5% annual growth, among the fastest in the restaurant sector. Furthermore, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Domino's provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

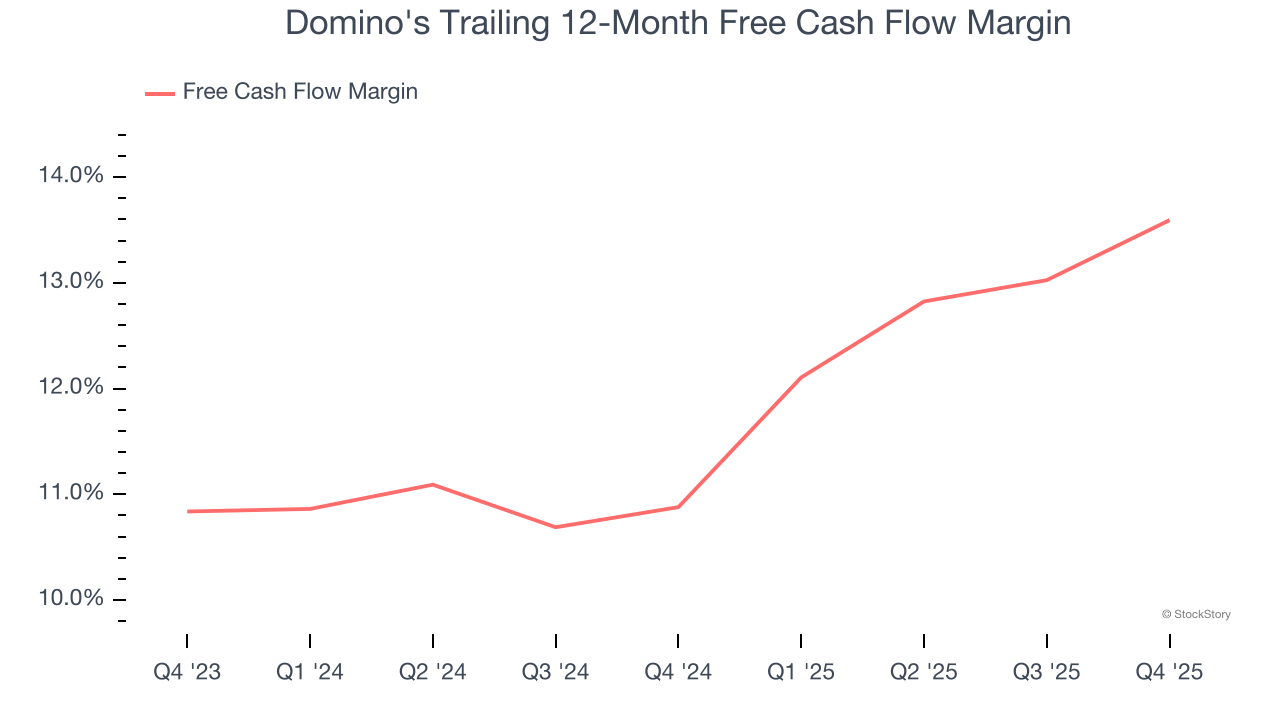

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Domino’s margin expanded by 2.7 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat. Domino’s free cash flow margin for the trailing 12 months was 13.6%.

One Reason to be Careful:

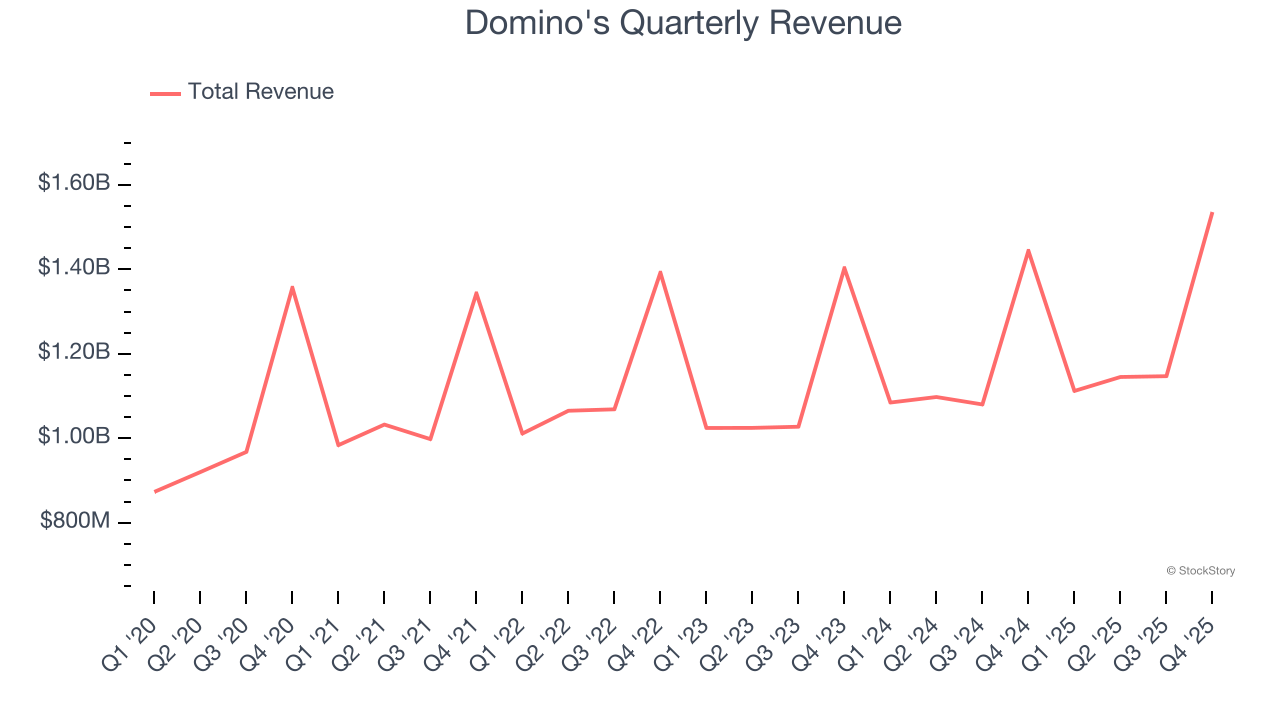

Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Domino’s 5.3% annualized revenue growth over the last six years was tepid. This wasn’t a great result compared to the rest of the restaurant sector, but there are still things to like about Domino's.

Final Judgment

Domino's has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 19.9× forward P/E (or $376.54 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Domino's

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.