Let’s dig into the relative performance of Take-Two (NASDAQ: TTWO) and its peers as we unravel the now-completed Q4 consumer internet earnings season.

The ways people shop, transport, communicate, learn and play are undergoing a tremendous, technology-enabled change. Consumer internet companies are playing a key role in lives being transformed, simplified and made more accessible.

The 46 consumer internet stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was in line.

While some consumer internet stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.5% since the latest earnings results.

Take-Two (NASDAQ: TTWO)

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ: TTWO) is one of the world’s largest video game publishers.

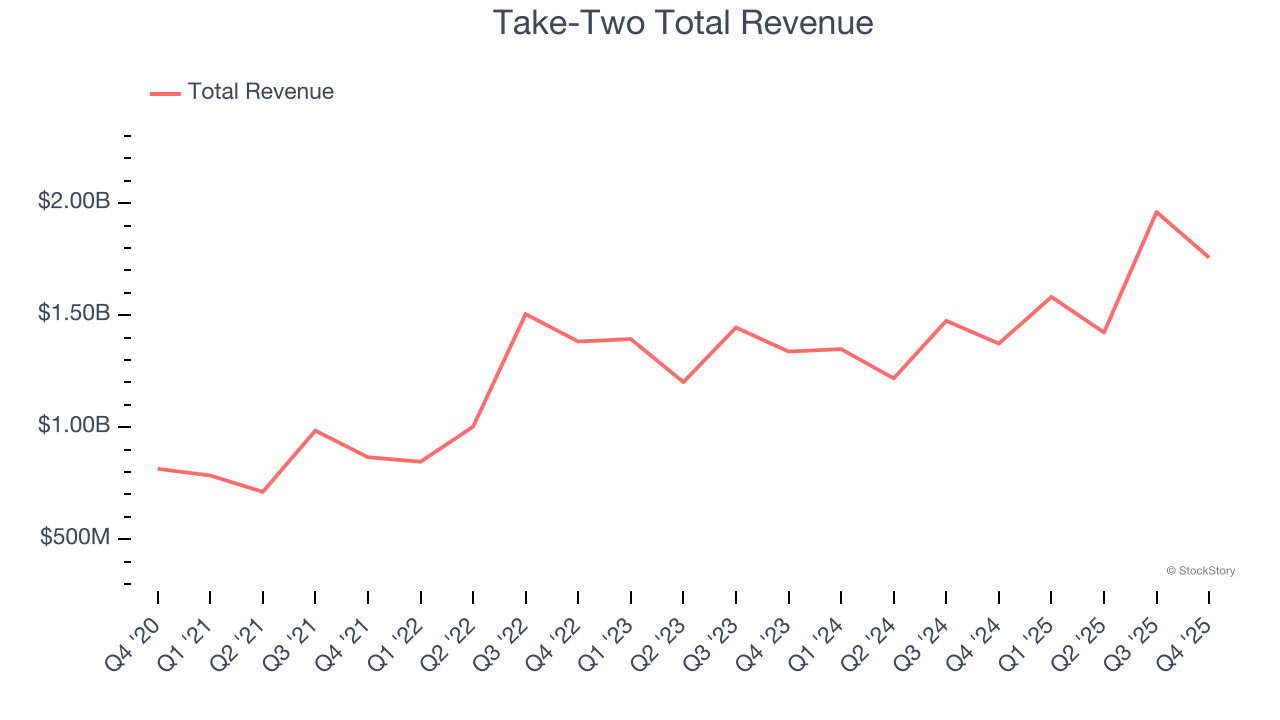

Take-Two reported revenues of $1.76 billion, up 27.9% year on year. This print exceeded analysts’ expectations by 11.2%. Overall, it was a satisfactory quarter for the company with a solid beat of analysts’ EBITDA estimates but full-year EBITDA guidance missing analysts’ expectations significantly.

Strauss Zelnick, Chairman and CEO of Take-Two Interactive, stated: “Our outstanding third quarter results reflect outperformance from all of our labels, and we are once again raising our Net Bookings outlook for Fiscal 2026. With ongoing momentum across many of our businesses, and the highly anticipated launch of Grand Theft Auto VI on November 19th, we continue to project record levels of Net Bookings in Fiscal 2027, which we believe will establish a new financial baseline for our business, set us on a path to enhanced profitability, and provide further balance sheet strength and flexibility.”

Take-Two delivered the weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 1.2% since reporting and currently trades at $209.68.

Is now the time to buy Take-Two? Access our full analysis of the earnings results here, it’s free.

Best Q4: LendingTree (NASDAQ: TREE)

Using the same comparison model that revolutionized travel booking, LendingTree (NASDAQ: TREE) operates an online platform that connects consumers with financial service providers across mortgages, personal loans, credit cards, insurance, and other financial products.

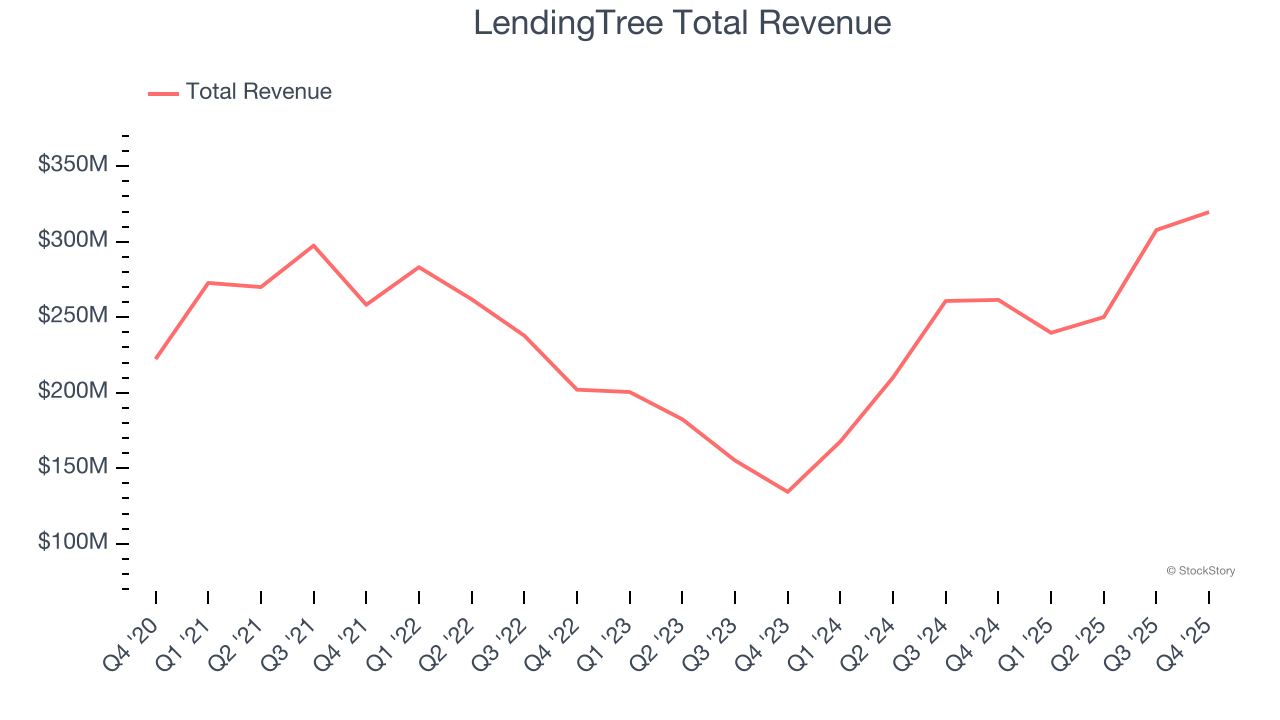

LendingTree reported revenues of $319.7 million, up 22.2% year on year, outperforming analysts’ expectations by 11.5%. The business had an incredible quarter with EBITDA guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

LendingTree scored the highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 7.6% since reporting. It currently trades at $40.60.

Is now the time to buy LendingTree? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Shutterstock (NYSE: SSTK)

Originally featuring a library that included many of founder Jon Oringer’s photos, Shutterstock (NYSE: SSTK) is now a digital platform where customers can license and use hundreds of millions of pieces of content.

Shutterstock reported revenues of $220.2 million, down 12% year on year, falling short of analysts’ expectations by 12.7%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Shutterstock delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 5.6% since the results and currently trades at $16.30.

Read our full analysis of Shutterstock’s results here.

Electronic Arts (NASDAQ: EA)

Best known for its Madden NFL and FIFA sports franchises, Electronic Arts (NASDAQ: EA) is one of the world’s largest video game publishers.

Electronic Arts reported revenues of $3.05 billion, up 37.5% year on year. This number surpassed analysts’ expectations by 4%. Overall, it was a very strong quarter as it also put up an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ revenue estimates.

The stock is flat since reporting and currently trades at $199.50.

Read our full, actionable report on Electronic Arts here, it’s free.

Uber (NYSE: UBER)

Notoriously funded with $7.7 billion from the Softbank Vision Fund, Uber (NYSE: UBER) operates a platform of on-demand services such as ride-hailing, food delivery, and freight.

Uber reported revenues of $14.37 billion, up 20.1% year on year. This print met analysts’ expectations. Taking a step back, it was a mixed quarter as it failed to impress in some other areas of the business.

The company reported 202 million users, up 18.1% year on year. The stock is down 4.5% since reporting and currently trades at $74.45.

Read our full, actionable report on Uber here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.