Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Sleep Number (NASDAQ: SNBR) and its peers.

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

The 4 home furniture retailer stocks we track reported a slower Q1. As a group, revenues along with next quarter’s revenue guidance were in line with analysts’ consensus estimates.

In light of this news, share prices of the companies have held steady as they are up 3.3% on average since the latest earnings results.

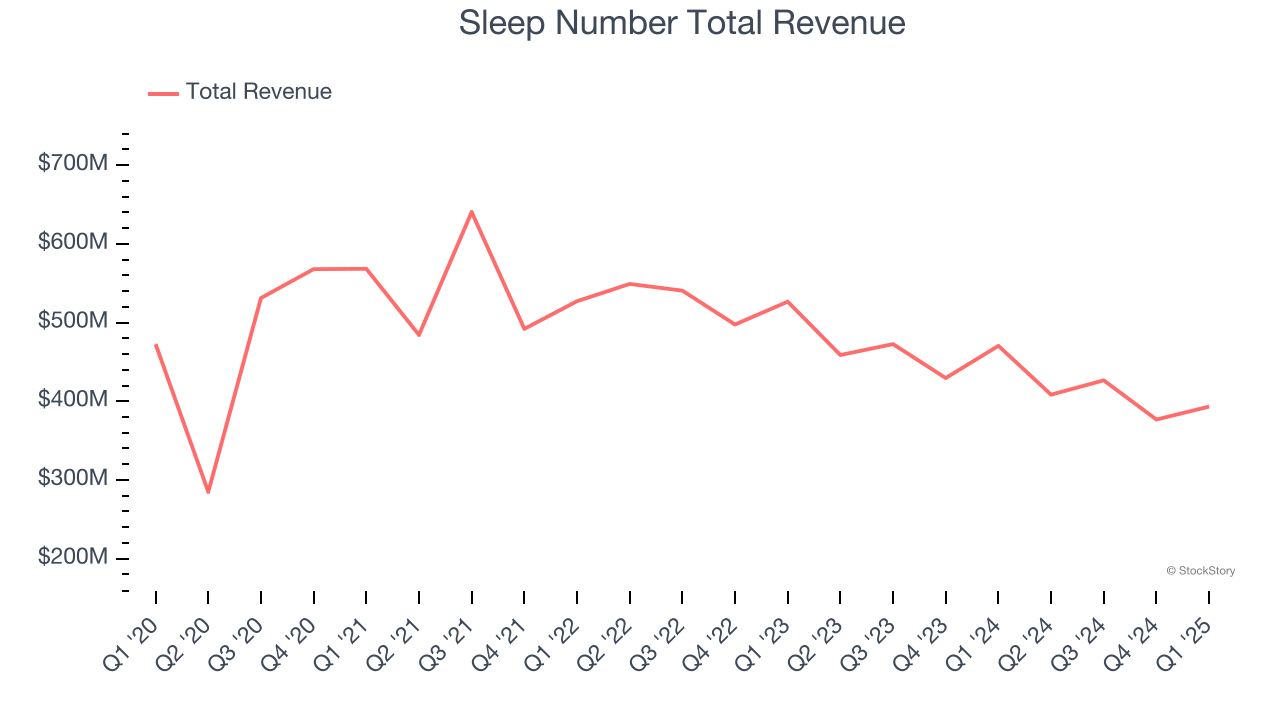

Slowest Q1: Sleep Number (NASDAQ: SNBR)

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ: SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

Sleep Number reported revenues of $393.3 million, down 16.4% year on year. This print fell short of analysts’ expectations by 1.2%. Overall, it was a softer quarter for the company with a significant miss of analysts’ EBITDA and EPS estimates.

Linda Findley, President and CEO, commented, “We are laser focused on delivering strong returns for shareholders and are taking a different approach to the Sleep Number business. I see a way to run our business on a lower cost basis without compromising our topline. We are fundamentally changing how we operate. We implemented an organizational redesign, including changes to our leadership team, to simplify decision making and bring us closer to the customer. With that change, we reduced corporate management roles by 21%. In addition, we are reshaping key functions within the company, including marketing and research and development, to further drive efficiency. Since I joined three weeks ago, our efforts have reduced second quarter operating expenses by approximately 10% of our current cost structure, as of the first quarter of 2025. "

Sleep Number delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. Unsurprisingly, the stock is down 9.6% since reporting and currently trades at $7.04.

Read our full report on Sleep Number here, it’s free.

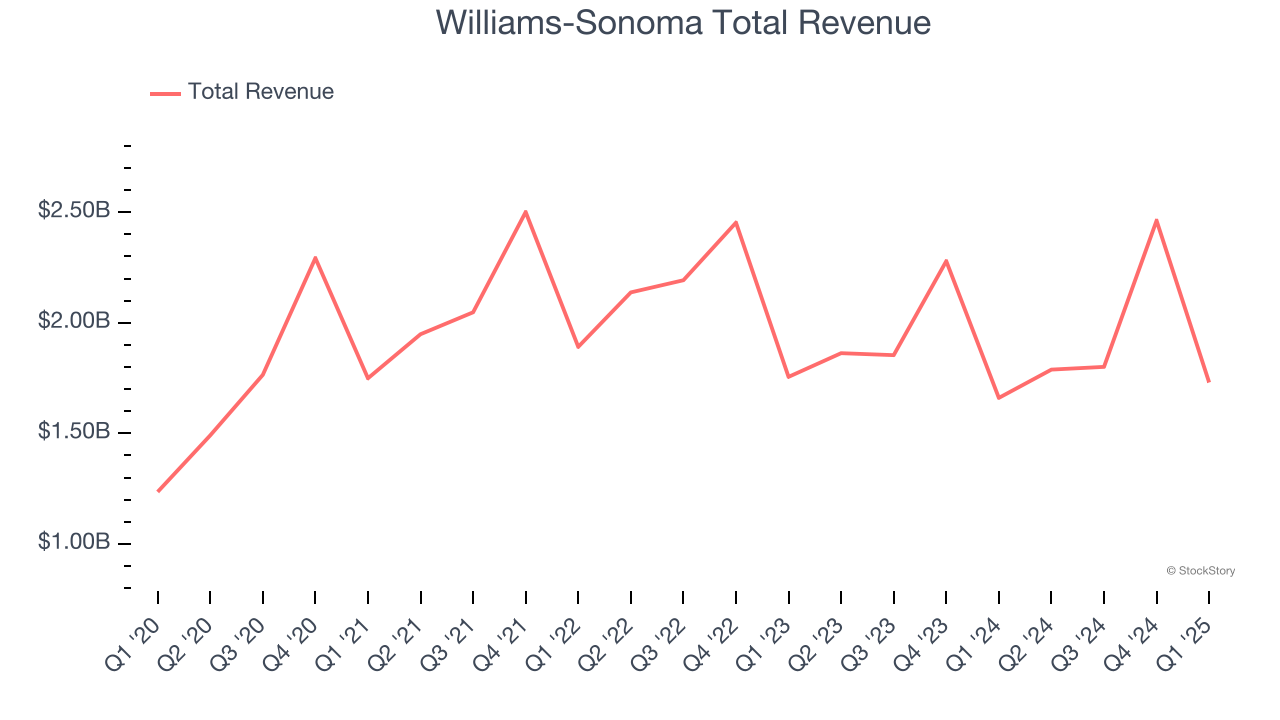

Best Q1: Williams-Sonoma (NYSE: WSM)

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE: WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

Williams-Sonoma reported revenues of $1.73 billion, up 4.2% year on year, outperforming analysts’ expectations by 4%. The business had a strong quarter with a decent beat of analysts’ EBITDA estimates.

Williams-Sonoma pulled off the biggest analyst estimates beat among its peers. The market seems content with the results as the stock is up 1.3% since reporting. It currently trades at $169.84.

Is now the time to buy Williams-Sonoma? Access our full analysis of the earnings results here, it’s free.

Arhaus (NASDAQ: ARHS)

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ: ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

Arhaus reported revenues of $311.4 million, up 5.5% year on year, falling short of analysts’ expectations by 0.8%. It was a softer quarter as it posted full-year EBITDA guidance missing analysts’ expectations significantly and a significant miss of analysts’ EBITDA estimates.

Interestingly, the stock is up 7.7% since the results and currently trades at $9.02.

Read our full analysis of Arhaus’s results here.

RH (NYSE: RH)

Formerly known as Restoration Hardware, RH (NYSE: RH) is a specialty retailer that exclusively sells its own brand of high-end furniture and home decor.

RH reported revenues of $814 million, up 12% year on year. This number lagged analysts' expectations by 0.6%. Taking a step back, it was a mixed quarter as it also logged a solid beat of analysts’ EPS estimates but a significant miss of analysts’ EBITDA estimates.

RH pulled off the fastest revenue growth among its peers. The stock is up 13.8% since reporting and currently trades at $201.48.

Read our full, actionable report on RH here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.