Calavo’s 18.2% return over the past six months has outpaced the S&P 500 by 12.8%, and its stock price has climbed to $26.61 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Calavo, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Calavo Will Underperform?

We’re glad investors have benefited from the price increase, but we're cautious about Calavo. Here are three reasons why there are better opportunities than CVGW and a stock we'd rather own.

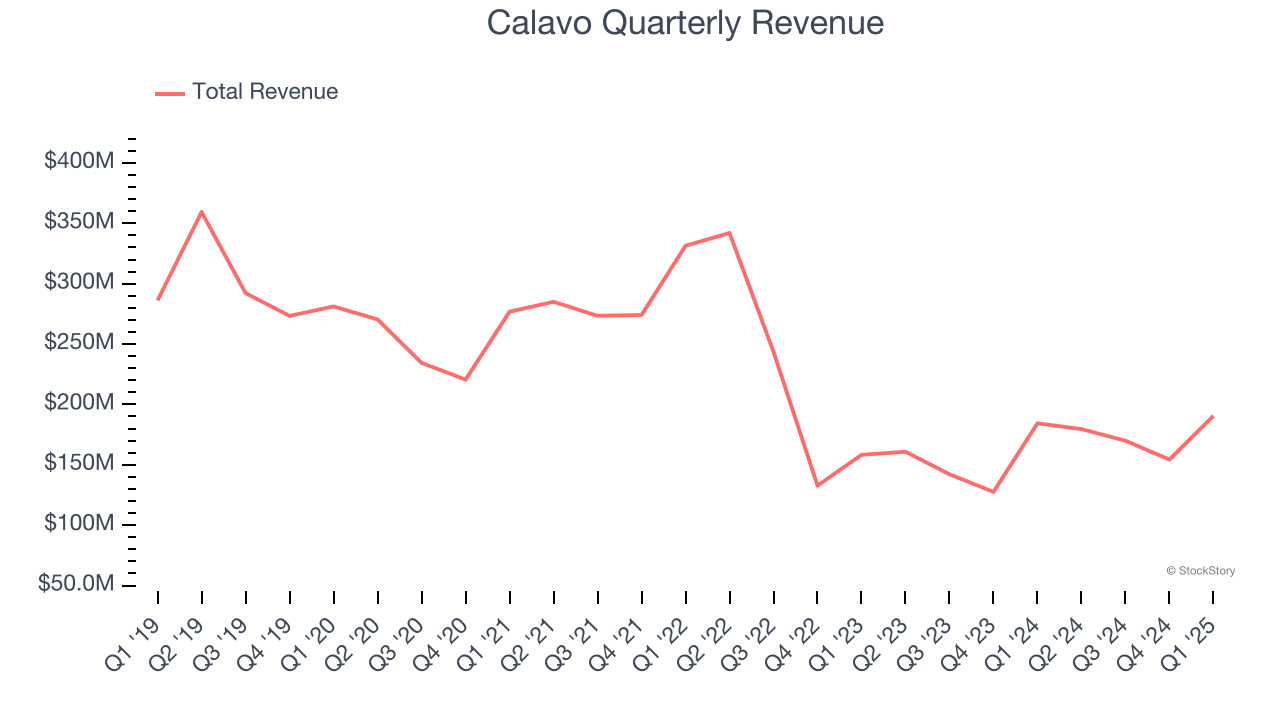

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Calavo’s demand was weak and its revenue declined by 15.8% per year. This was below our standards and signals it’s a low quality business.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Calavo’s revenue to drop by 1.8%. it’s tough to feel optimistic about a company facing demand difficulties.

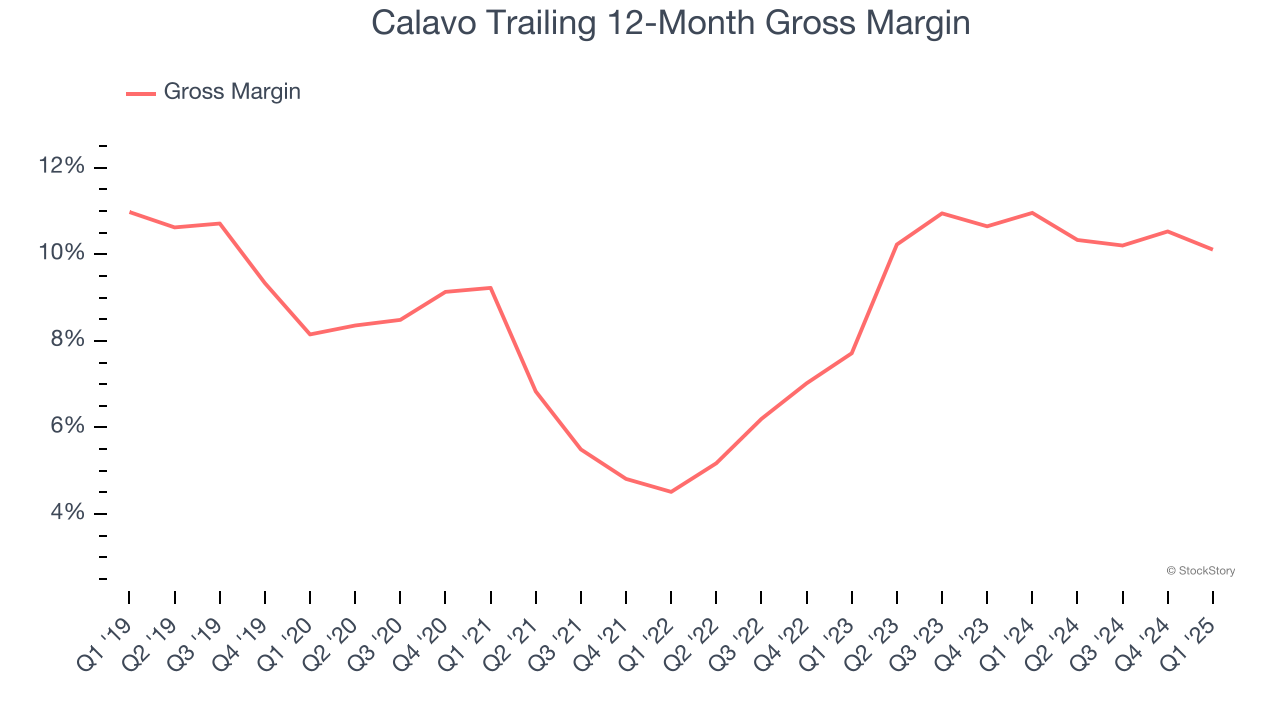

3. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Calavo has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 10.5% gross margin over the last two years. That means Calavo paid its suppliers a lot of money ($89.49 for every $100 in revenue) to run its business.

Final Judgment

Calavo falls short of our quality standards. With its shares topping the market in recent months, the stock trades at 14.1× forward P/E (or $26.61 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are more exciting stocks to buy at the moment. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of Calavo

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.