AXIS Capital has had an impressive run over the past six months. While the S&P 500 has been flat, the stock has returned 11.1% and now trades at $100.49. This run-up might have investors contemplating their next move.

Is now the time to buy AXIS Capital, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is AXIS Capital Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about AXIS Capital. Here are three reasons why we avoid AXS and a stock we'd rather own.

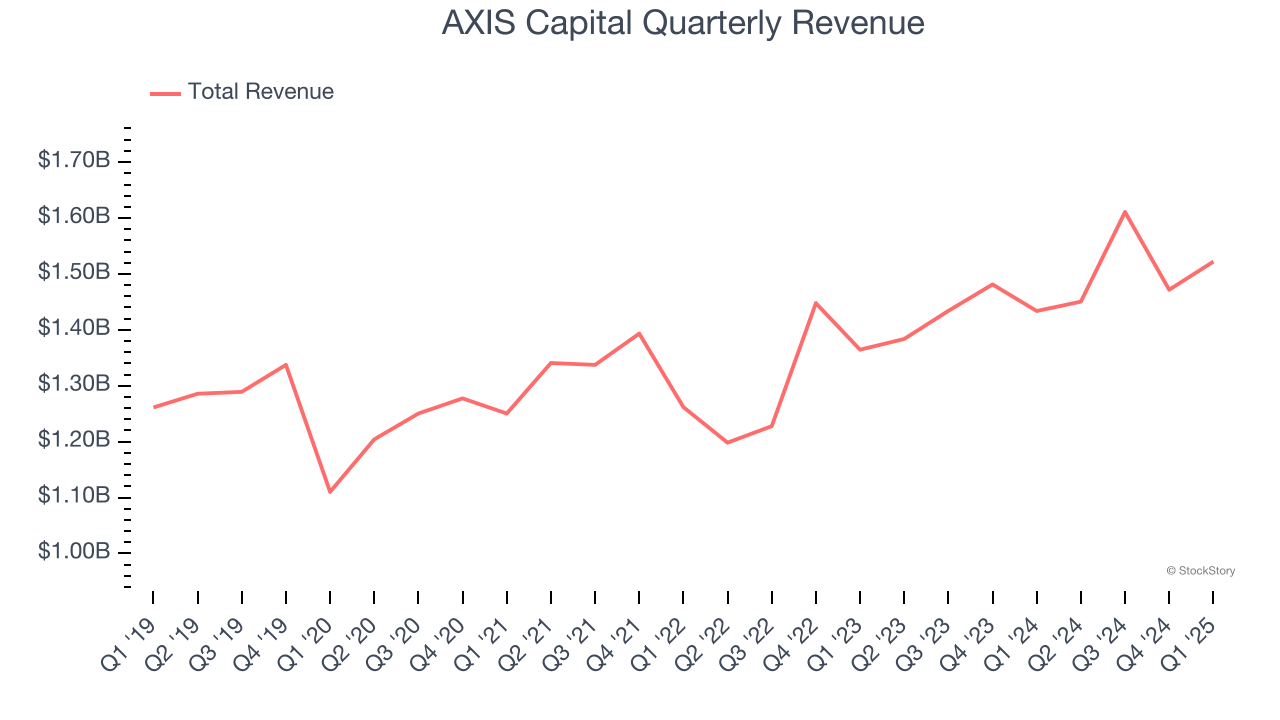

1. Long-Term Revenue Growth Disappoints

Big picture, insurers generate revenue from three key sources. The first is the core business of underwriting policies. The second source is income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services.

Regrettably, AXIS Capital’s revenue grew at a sluggish 3.8% compounded annual growth rate over the last five years. This fell short of our benchmark for the insurance sector.

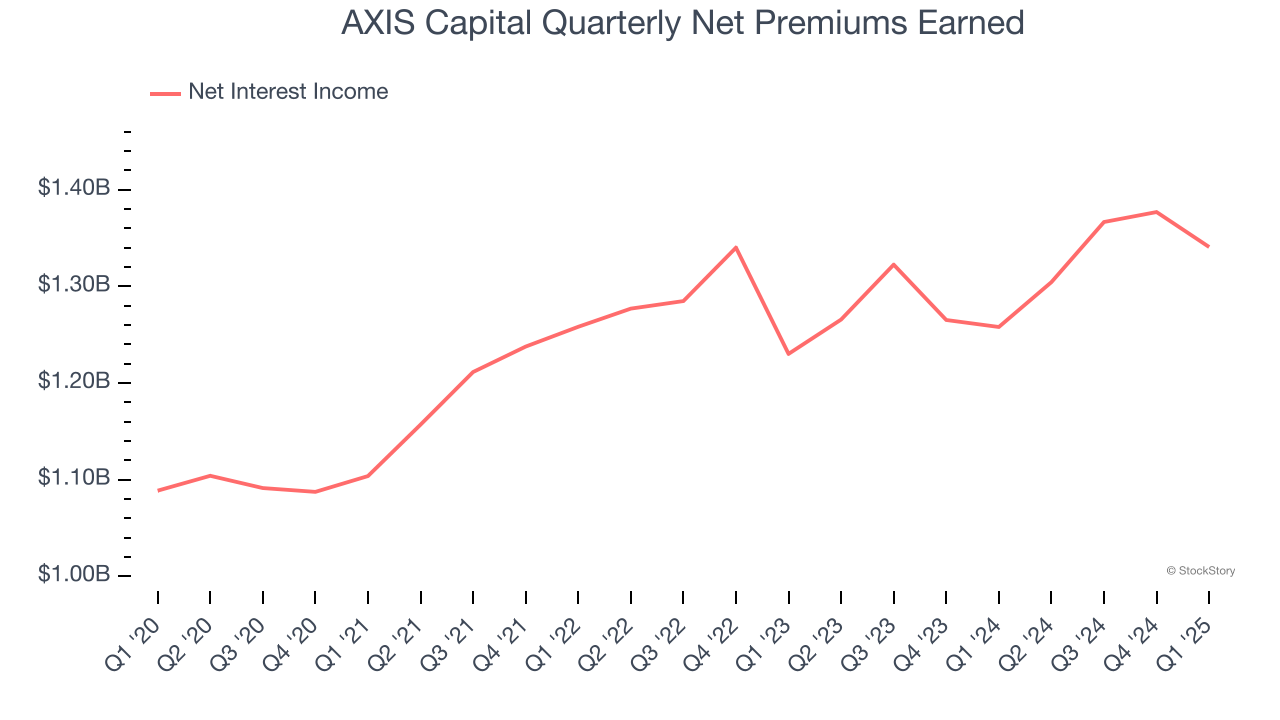

2. Net Premiums Earned Points to Soft Demand

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

AXIS Capital’s net premiums earned has grown at a 2.5% annualized rate over the last two years, much worse than the broader insurance industry and slower than its total revenue.

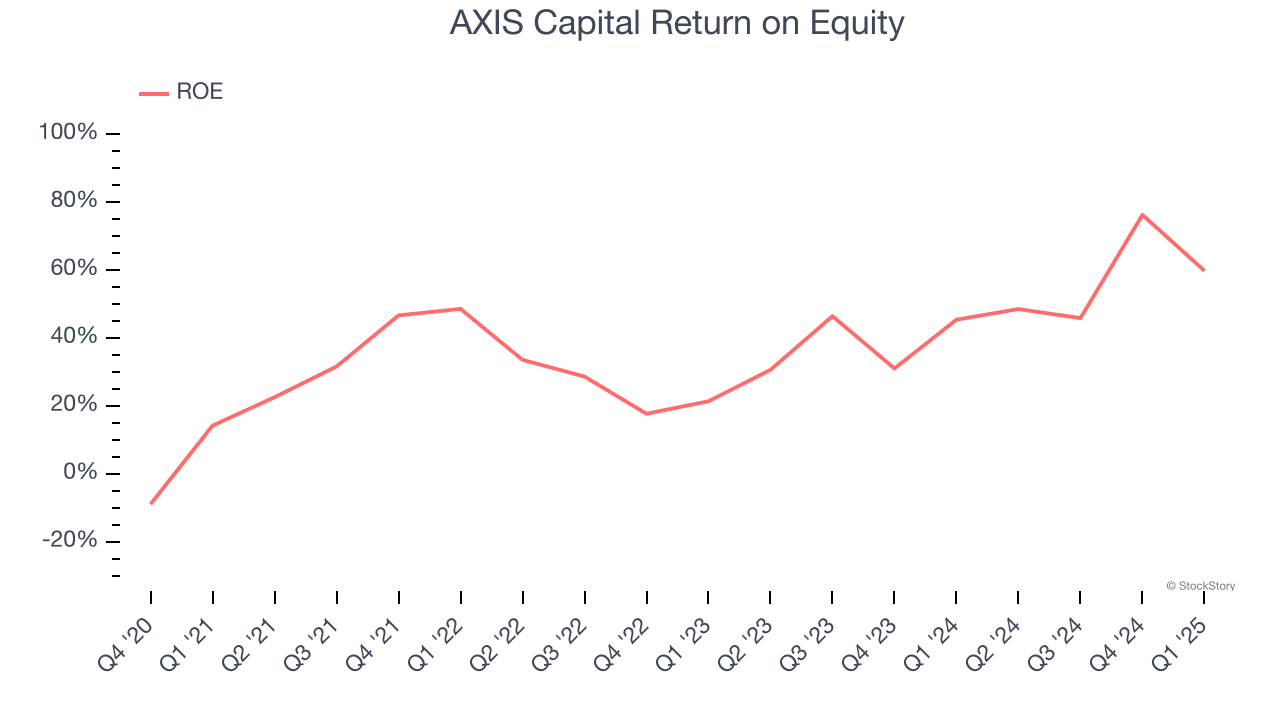

3. Previous Growth Initiatives Haven’t Impressed

Return on Equity, or ROE, ties everything together and is a vital metric. It tells us how much profit the insurer generates for each dollar of shareholder equity entrusted to management. Over a long period, insurers with higher ROEs tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, AXIS Capital has averaged an ROE of 9.5%, uninspiring for a company operating in a sector where the average shakes out around 7.5%. This shows AXIS Capital has a weak competitive moat.

Final Judgment

AXIS Capital isn’t a terrible business, but it doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 1.4× forward P/B (or $100.49 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our top digital advertising picks.

Stocks We Would Buy Instead of AXIS Capital

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.