Over the past six months, Baxter’s stock price fell to $36.42. Shareholders have lost 7.3% of their capital, which is disappointing considering the S&P 500 has climbed by 1.5%. This might have investors contemplating their next move.

Is now the time to buy Baxter, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even with the cheaper entry price, we're cautious about Baxter. Here are three reasons why BAX doesn't excite us and a stock we'd rather own.

Why Do We Think Baxter Will Underperform?

Founded in 1931, Baxter International (NYSE: BAX) develops, manufactures, and sells a range of medical products and therapies, focusing on critical care, renal care, hospital products, and advanced surgical solutions.

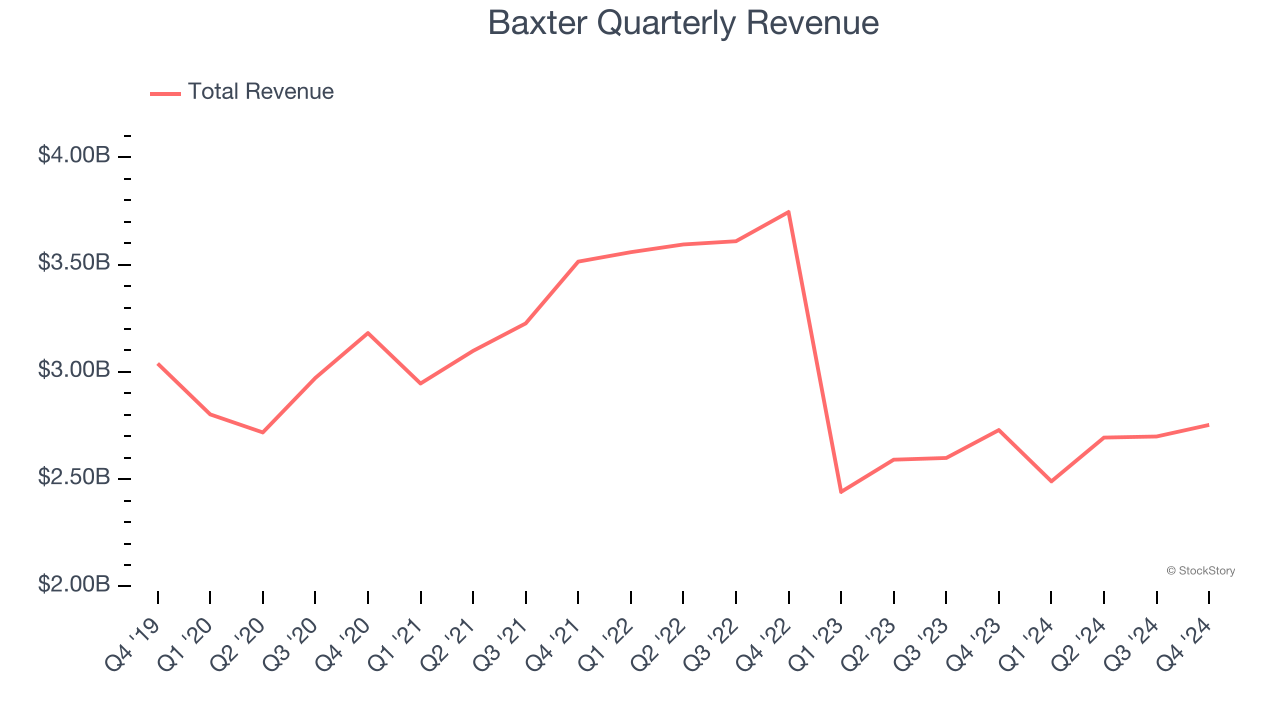

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Baxter’s demand was weak over the last five years as its sales fell at a 1.3% annual rate. This wasn’t a great result and signals it’s a low quality business.

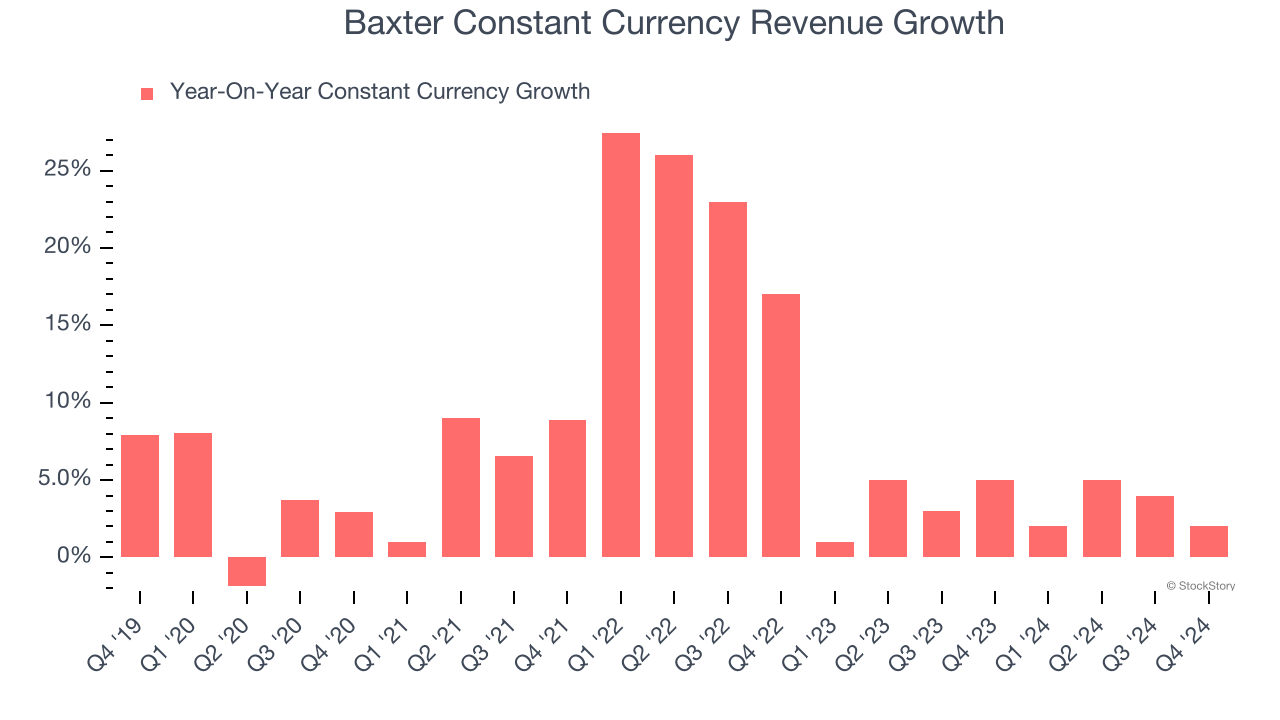

2. Weak Constant Currency Growth Points to Soft Demand

We can better understand Medical Devices & Supplies - Diversified companies by analyzing their constant currency revenue. This metric excludes currency movements, which are outside of Baxter’s control and are not indicative of underlying demand.

Over the last two years, Baxter’s constant currency revenue averaged 3.4% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

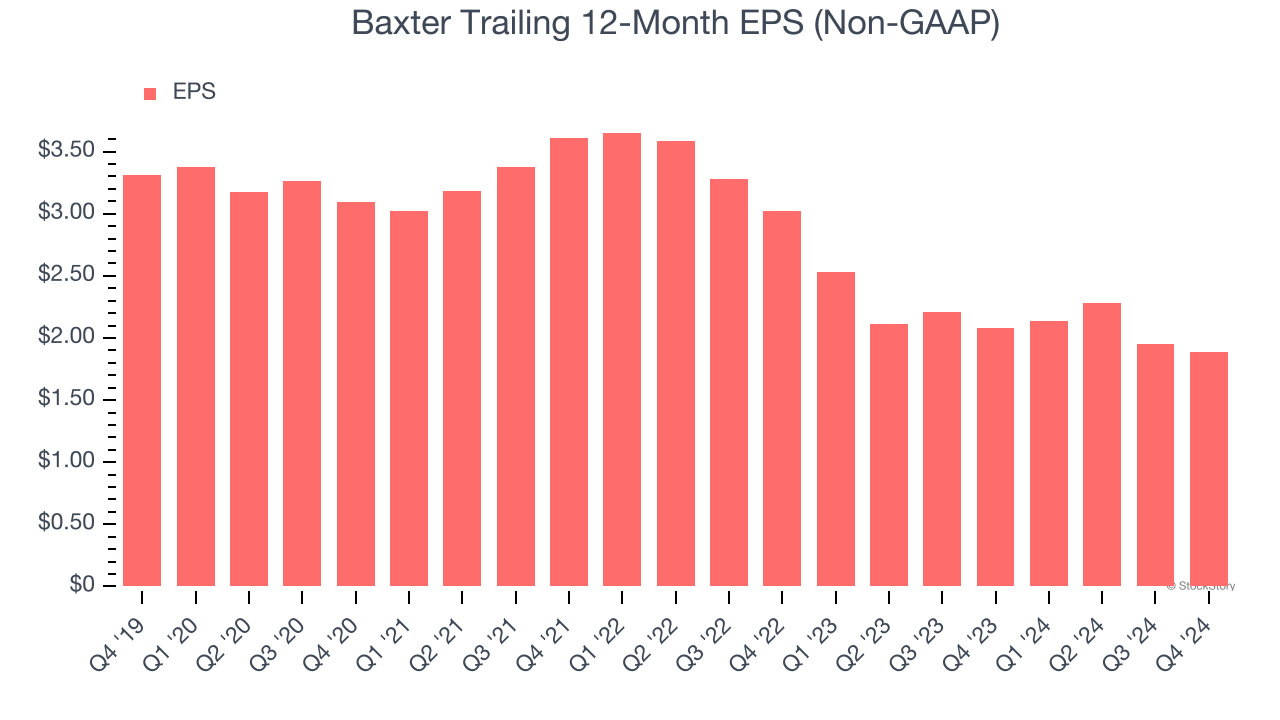

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Baxter, its EPS declined by 10.7% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Baxter doesn’t pass our quality test. Following the recent decline, the stock trades at 14.8× forward price-to-earnings (or $36.42 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Baxter

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.