Alignment Healthcare has been on fire lately. In the past six months alone, the company’s stock price has rocketed 60.1%, reaching $13.88 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Alignment Healthcare, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the momentum, we're sitting this one out for now. Here are three reasons why there are better opportunities than ALHC and a stock we'd rather own.

Why Is Alignment Healthcare Not Exciting?

Founded in 2013, Alignment Healthcare (NASDAQ: ALHC) provides Medicare Advantage plans with a focus on technology such as telemedicine and a proprietary platform that digitizes care coordination and features predictive analytics.

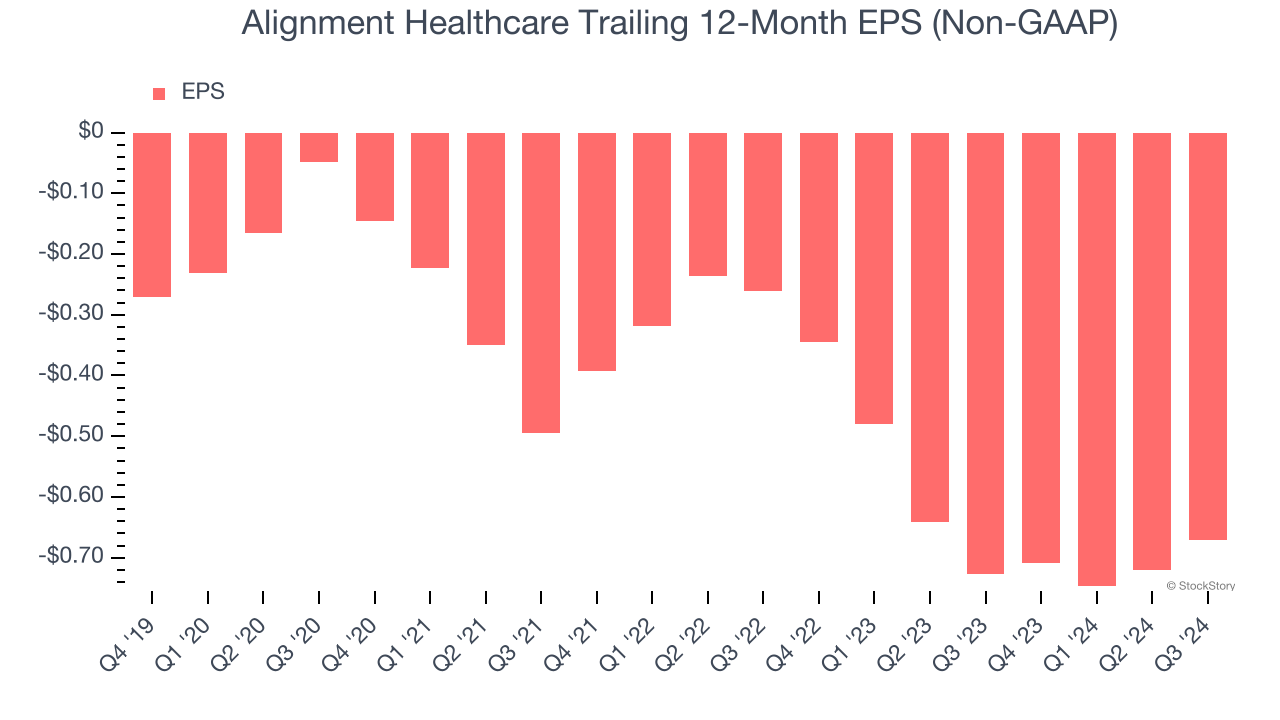

1. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Alignment Healthcare’s earnings losses deepened over the last five years as its EPS dropped 24.5% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

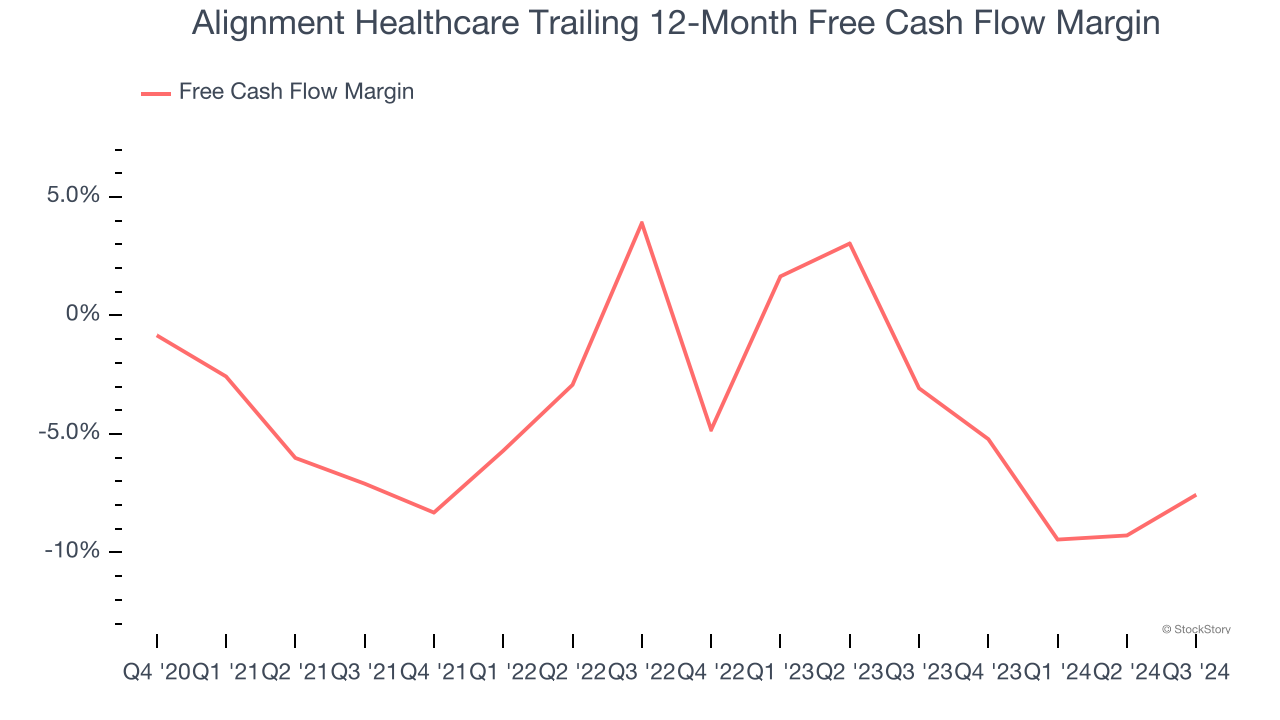

2. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Alignment Healthcare posted positive free cash flow this quarter, the broader story hasn’t been so clean. Alignment Healthcare’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 3.5%. This means it lit $3.50 of cash on fire for every $100 in revenue.

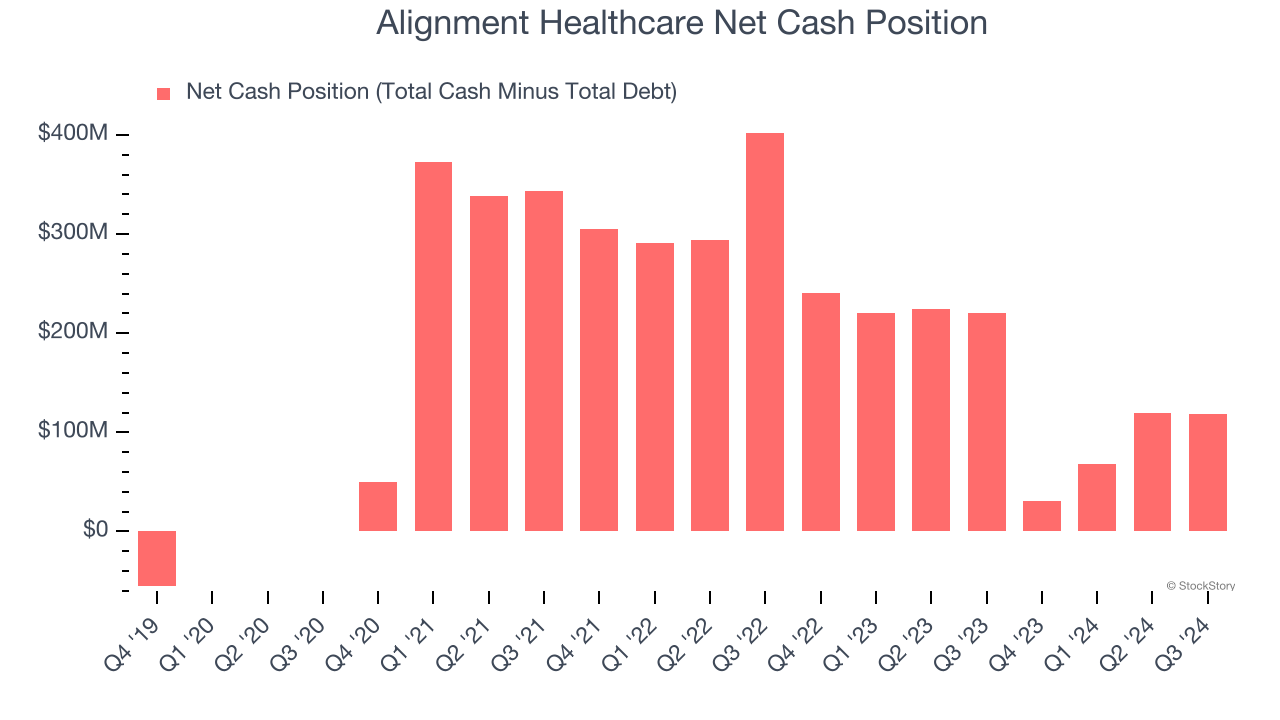

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Alignment Healthcare burned through $186.7 million of cash over the last year. With $340.3 million of cash on its balance sheet, the company has around 22 months of runway left (assuming its $221.8 million of debt isn’t due right away).

Unless the Alignment Healthcare’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Alignment Healthcare until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

Alignment Healthcare isn’t a terrible business, but it doesn’t pass our quality test. Following the recent rally, the stock trades at 79.8× forward EV-to-EBITDA (or $13.88 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Alignment Healthcare

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.