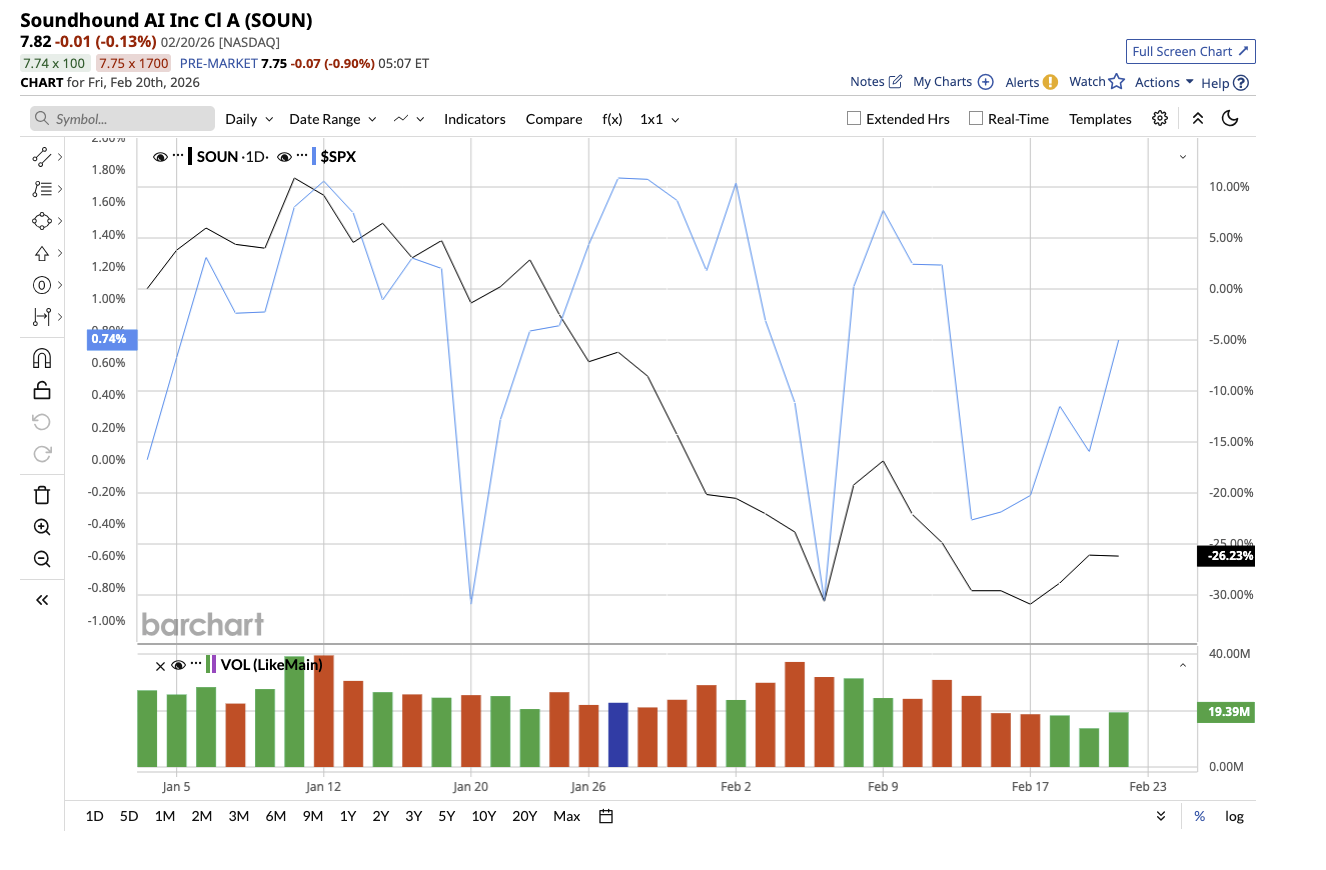

SoundHound AI (SOUN), a pure-play voice artificial intelligence company, operates in one of the most exciting corners of the AI market. Yet, it is down 26% so far this year and 64% below its 52-week high, weighed down by concerns over profitability, excessive cash burn, shareholder dilution, and a broader market shift away from unprofitable growth stocks. The company will report its third-quarter earnings on Feb. 26. Even a modest surprise in the quarter can have a significant impact on the stock.

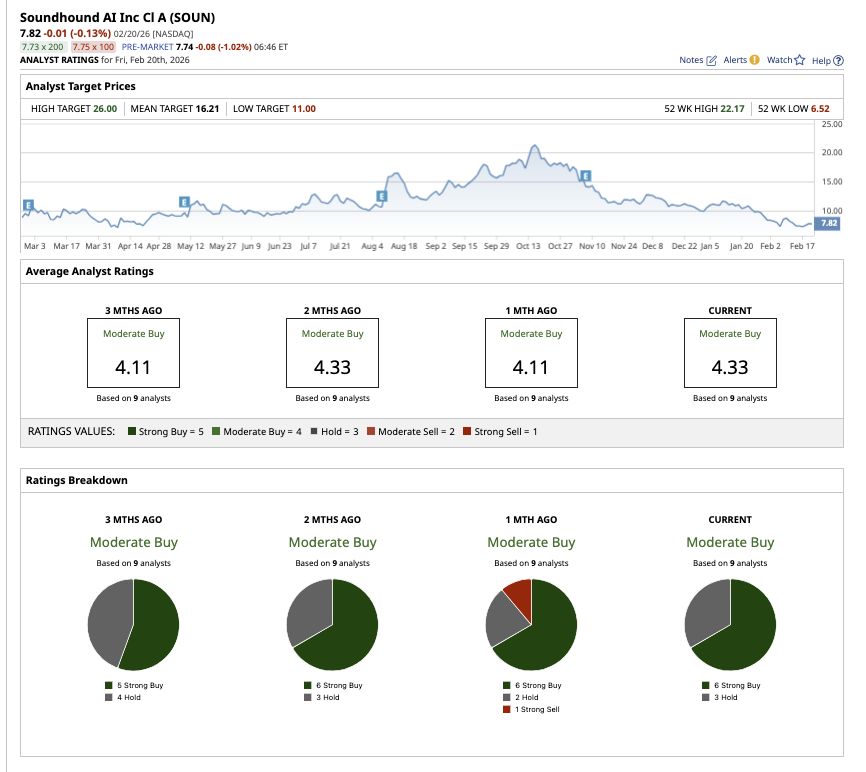

While SOUN stock currently trades at about $7.80 per share, analysts have assigned a high price estimate of $26, implying that the stock can rally as much as 233%.

Will a strong quarter drive this surprise potential?

Fundamentals Aren't SoundHound AI's Problem

Valued at $3.2 billion, SoundHound AI is a mid-cap company that builds conversational AI software enabling businesses to power voice assistants in cars, restaurants, customer service platforms, and other connected devices. The company continues to report robust sales growth and a solid net revenue retention rate over 100%, which shows the company is retaining and growing customers.

In the second quarter, SoundHound reported a staggering 217% year-over-year (YoY) increase in revenue to $42.7 million, marking the company’s highest quarterly revenue to date. During the quarter, approximately 3 billion inquiries were handled, more than doubling YoY volume, and the platform's monthly volume reached 1 billion queries. The company saw significant expansion across automotive, enterprise AI customer service, and restaurant AI and automation. Polaris, SoundHound’s proprietary multimodal, multilingual speech foundation model, has been a key driver of this growth, delivering over 35% accuracy and 4x latency while running at a reduced cost. Polaris is now being integrated across acquisitions such as Synq3 and Amelia, which management expects to improve gross margins sequentially and boost client retention.

CEO Keyvan Mohajer emphasized that prior acquisitions are now showing outsized returns, turning pre-merger decline into post-merger growth within 12 to 18 months. So, the recent stock decline isn’t because SoundHound’s fundamentals have collapsed but rather a valuation reset. The company is still operating in the red. In Q2, it reported an adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) loss of $14.3 million and an adjusted net loss of $11.9 million. Adjusted gross margin stood at 58%.

SoundHound’s newly launched Amelia 7 agentic AI platform is an emerging opportunity that could turn the bottom line green. According to the management, 15 large enterprise customers are being migrated onto the platform. Additionally, the net revenue retention rate has jumped from below 90% to over 120%. At the end of the quarter, the company had no debt and a $230 million cash balance.

Management raised the revenue guidance for the full year to a range between $160 million and $178 million, which implies demand isn’t the problem. The company also expects adjusted EBITDA profitability by the end of 2025. However, EBITDA is not a true measure of profit, and the company is still generating negative free cash flow. The good news is that achieving adjusted EBITDA profitability is a significant step forward. It means that SoundHound's operating leverage is improving, reducing the risk of massive cash burn

Why Feb. 26 Is Important for SOUN Stock

This earnings report is a crucial test for the company. If SoundHound can show accelerating enterprise adoption, faster-than-expected EBITDA growth, improved cost discipline, or a clearer path to profitability, this beaten-down AI stock could deliver the upside that analysts expect. If you believe in the company’s turnaround story and are willing to handle the risk, this pullback presents a great opportunity to accumulate SOUN stock.

Overall, Wall Street is moderately bullish about SOUN stock. Out of the nine analysts covering SOUN, six rate it a “Strong Buy,” and three recommend a “Hold.” Its average target price of $16.21 suggests an upside potential of 107% from current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why Citi Analysts Think You Should Buy Microsoft Stock Now

- Domino's Pizza Hikes Its Dividend By 14.3% After Free Cash Flow Rises 29% - Value Buyers Love DPZ Stock

- Up 265% in the Past 5 Days, Is There Any More Upside Left for Rackspace Stock?

- CoreWeave’s Q4 Results Due Feb. 26: What It Means for CRWV Stock